Drivers continue to turn away from ICE cars as best ever year for electric cars continues (except Tesla)

Global EV Tracker: Insights from 40+ markets accounting for 85% of car sales.

This issue of New AutoMotive’s Global EV Tracker covers car registrations up to the end of February 2025. We hope you enjoy our take on the latest moves in EV registrations around the globe. Don’t forget that you can always dig through the numbers yourself….

Fuel type overview

As we indicated last month, the first two months of each year - the end of one Chinese year and the start of a new year - are typically a low point for the Chinese battery electric market. As the world’s largest car market, this can drag down global results.

However, the year of the wood snake has seen good fortune for battery electric and a new harvest for uptake of plug-in hybrid registrations, as each have had their best ever start to the year. Pure electric car registrations reached 1.4m in the first two months of the year - 170,000 (13%) up on the first two months of 2024, whilst plug-in hybrids hit 0.7m - 215,000 (44%) up on the same time last year, rewarding makers who shed their petrol and diesel skins as the days warm (in the northern hemisphere at least).

Meanwhile ICE cars were unable to tempt buyers and slithered downward to yet another new post-pandemic low - falling 7% (450,000) to 6.1m, as makers who cunningly failed to invest in the transition reap the consequences. In fact it was only rising BEV and PHEV registrations which meant car sales increased at all.

OK, that’s enough zodiacal snake metaphors. Let’s wind forward to the round-up.

You’re receiving this because you signed up to receive updates from us. Changed your mind? Not a problem, you can change your preferences or opt out of emails here.

The Headlines

In February 2025:

729,000 battery-electric cars were registered, the highest February total ever recorded and a 176,000 (32%) rise on the same month in 2024.

The rise was led by China, with an increase of 121,000 EVs; the USA, defying doomsters with a 20,000 increase; Germany returning to pre-sales crash levels with 8,000 extra registrations, and the UK continuing to power ahead, with an additional 5,700.

In China, registrations of plug-in hybrids surged even more strongly, resulting in an increase of 273,000 (more than 62%) in cars with a plug on the same month last year

Globally, cars with a plug now account for more than 22.7% of registrations - up 32% (5.5 percentage points) on their market share last year. Flatlining? What flatlining?

Don’t forget that for more information, you can check out the Global EV Tracker dashboard - which allows you to produce customised analysis of car sales, market share and manufacturers - at the button below. Our new country profile pages, offering an overview of country-by-country policies and sales, are available at the same link.

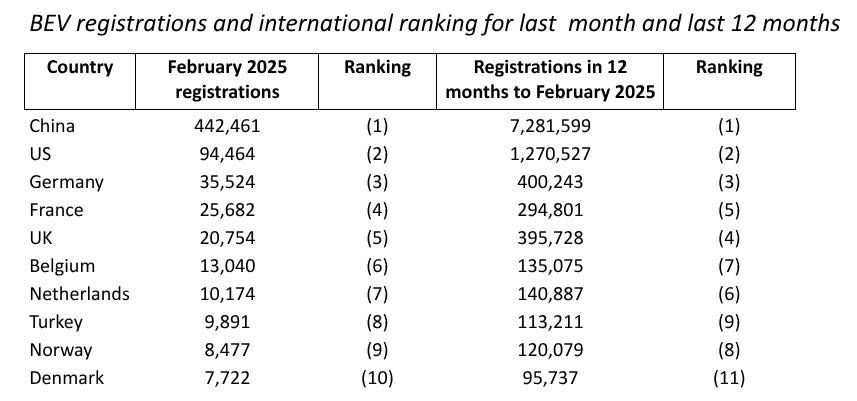

Market Indicators

What are the biggest markets for EV registrations?

China and the US are the two largest markets for EVs, as they are for other fuel types. Germany comfortably took third place this month, as sales continue their recovery, up by 8,000 on last February and its best month for more than a year.

France has briefly overtaken the UK as British buyers await the next round of number plates. As a strictly seasonal effect, we expect the positions to be reversed next month.

Turkey’s strong run has continued, and it is the third largest non-European EV market, although these registrations pre-date the recent constitutional crisis caused by the ruling party’s clampdown on opposition politicians.

Where are we seeing the greatest growth?

Taiwan’s market is dependent on imports, but its extraordinary growth is looking sustained. Registrations are up 63% in the 12 months to February 2024 on the preceding 12 months.

Iceland’s growth, in contrast, is more an artefact of comparing with February 2024 after a slump caused by a gigantically botched road-pricing scheme.

Czechia, Denmark and Norway are all beneficiaries of long term, stable incentives although Czechia is much earlier in its journey, with battery EV market share of 4%.

Meanwhile Spain’s recent growth has taken it to the edge of the top 10 largest EV markets, after years of lagging performance. (See Europe continent analysis below).

Where is EV market share highest?

The Nordic and Benelux nations hold 8 of the top 10 placings for market share in 2024. With the exception of Norway, which is set to ban ICE cars at the end of the year, all might expect to see continued further rises in 2025 with new tougher regulations, albeit a 3 -year averaging period until 2027.

Singapore’s surge has seen battery electric market share increase from 11% to 42% in 2 years. At this rate, they will have joined Norway in ending non-zero emission car sales by 2029. China’s battery EV registrations - which already exceed the rest of the world put together - follow a distinct saw tooth pattern, with January and February registrations particularly low. They are likely to rise further up the table as the year progresses (see Asia continent analysis below).

Continent Analysis

Americas

Whilst the federal tax credit and clean car mandates in 15 states remain in place, the Trump administration’s contradictory rhetoric on EVs does not appear to have unduly dissuaded USA car buyers. More than 94,000 battery EVs were registered, up 27% from the 74,000 registered in February 2024, whilst ICE car sales fell back 6%. However the biggest declines were seen in the PHEV market, which were down 19%. This reflects the continued divergence between China, where longer-range PHEVs have surged in popularity, whilst short-range US and European counterparts are starting to fall from favour.

Turning to Brazil, battery EV sales crept up to 2.7% in February, the best market share since May 2024. Hybrids account for another 3.6% - second only to January 2025 in the last 14 months. So the omens are good, but Brazil’s story of the switch has a lot further to run.

January and February are typically slow months for the whole car market in Mexico, and this applied as much to the battery EV market. Total car registrations were 118,000, the lowest since September - whilst at 1,302, battery electric registrations were at their lowest level since October 2023. This means it’s now the 7th month in a row that battery electric has tacked between 1 and 2% market share. Given the constant efforts of its northern neighbour to reshore manufacturing, Mexico’s best bet to break out of this range might be to boost demand with supply-side measures of the type used in Europe and China, and use its lower domestic labour costs to favour local manufacturers - using retaliatory tariffs where necessary.

Asia

After its traditional January spike, ICE car sales in China were sharply down again last month, with registrations dropping below 1 million a month for the first time since February 2024. Meanwhile we saw much bigger rises over the same period for both battery electric (up 38%, to 27% market share) and plug-in hybrid sales (up a whopping 132% to 16% market share), helped by a combination of continued central government trade-in incentives and fierce price competition of a level completely unseen in the European and US markets.

This supercharging of the PHEV sector - perhaps as the switch reaches out to more cautious majority drivers - is one key theme of the Chinese market in recent months. The other is the continued collapse in ICE as a fuel type, its market share falling by a steady 8 to 9 percentage points each year from 92% in 2021, to 57% today. Give people attractive, clean cars at good prices, and generations of attachment to polluting, inefficient cars which are expensive to run and need lots of repairs seems to mysteriously melt away. Funny that.

Tesla’s woes continue with a fourth placing for battery EV sales this month. Wuling, a joint venture 44% owned by General Motors, pushed it out of the top 3, the first time this has happened since April 2022. We’ll know in a month or two whether this was a blip, but it’s already an extended blip. Tesla’s 3 month rolling average registrations are down 17% on the same period last year, whilst every other manufacturer in the top 10 saw battery EV registrations rise, six of them (including BYD, Geely and Wuling) by more than 25%.

Meanwhile BMW were 16th in February with 4,600 registrations (97,000 across the past 12 months), whilst Volkswagen - for so long in the top 10 EV makers in China - are down to 20th.

The strategy of the European makers is becoming harder to grasp. 2 months into the Trump presidency, it’s clear that auto firms need to be hedged against daily policy and trade ructions in the US market. And fishing for ICE sales is a strictly short-term strategy in China, the world’s largest market - this pond will have dried up altogether in 5 years. Simultaneously, a lack of investment means they’re being wiped out of the rapidly expanding EV market by superior domestic products. The European makers’ response to these challenges is to lobby to be allowed to sell more cars in their home market of the type they can’t shift elsewhere. Is this a deliberate policy of retrenchment amid an acceptance of sales decline, or just astonishingly short-sighted?

Turning to other Asian markets, Thailand saw total sales slip back 25% on a huge January. Registrations of all fuel types fell, but battery electric was hit harder, sliding back to the 12% level it operated in through much of 2024.

It’s hard to identify seasonality in Thailand’s very volatile market. Rather what seems to be happening is a mix of economic factors and a prising of demand away from traditionally dominant Japanese makers towards Chinese firms. Aion, BYD, Changan, Chery, Great Wall and Vietnamese maker Vinfast are all planning - or have already opened - factories. We will have more idea next month whether these results are a blip after the bonanza month of January, or whether the bonanza was itself a blip.

The Singapore market is very clearly not experiencing a blip, as battery EV market share continues to steadily rise. February 2025, like pretty much every month, saw a new all-time high, with fully electric market share reaching 42%. BYD remain dominant amongst discriminating and well-heeled Singaporean car-buyers, with 50% market share, whilst Tesla and BMW trail on 16% and 7% market share respectively. Whilst diesel has disappeared, petrol’s toehold - whether amongst skeptics or status signallers - remains steady at a little below 20%, where it has been since early 2024. Battery electric is now cannibalising hybrid market share, which is down 17% in the past 12 months.

The transition in Turkey is a little behind Singapore, but going at quite a clip. Battery EV market share was 14% (9,891 registrations) in February, double the level seen in February 2024 in a market which was flat overall. This places it 9th in the leading global markets for battery electric cars. The wipeout of ICE is if anything accelerating, closing another door to manufacturers who haven not prepared for the transition. From February 2023 to February 2024, diesel market share halved from 20% to 10%. More recently it has been petrol’s turn to haemorrhage buyers, falling from 66% market share to 46% over the last 12 months. Whilst diesel has held steady more recently, the overall market share of ICE cars looks almost certain to dip below 50% later this year.

Taiwan is another car market which traditionally has a slow second month of the year, with annual troughs in total car registrations every February since 2019. However battery electric registrations comfortably survived that slump this month, with just over 2,000 registrations and 8.3% market share, both up by a factor of 3 on February 2024. In a market with a lot of month-to-month noise, and facing deep geopolitical uncertainty, the two constants are the accelerating decline of petrol, down from 67% to 58% in 12 months, and the rise of hybrids and batteries, up from 31% to 40%.

Meanwhile in India, battery electric sales remain stuck in reverse, baffling pronouncements from Transport Ministers notwithstanding. Market share of 4-wheelers is down to 0.99%, a fresh low, and even hybrid registrations are falling. Dead-end alternative fuels such as LPG and biofuels are the only growth sector, taking most of their market share from petrol cars. We should be well past these interim 5-10%-emissions-saving technologies now. With a long-standing commitment to all cars being zero emission by 2040 as a member of the Accelerating to Zero Coalition, India has got a low-emissions train to catch.

Finally Japan also remains stuck in a very persistent reverse gear, as it heads towards a second period of economic isolation first pioneered by the shoguns of the 17th century. In fact the last time around they stayed in touch with Korea and China, but even that looks to be off the cards this time around. It didn’t end well last time with technological stagnation, and that’s the story this century too. Market share in February was 1.0%, with more than three-quarters of the EV registered being imported.

Europe

The best ever start to European battery electric registrations continues, with February registrations up 28% across the EU and 31% across Europe as a whole (the EU-27 + the UK, Switzerland, Norway and Iceland) in the year to date on the same period last year, and 24% and 26% respectively in February alone.

Registrations rose in 25 markets - with big rises in the larger markets of Germany (31%), Italy (38%), Belgium (39%) and Spain (61%), alongside many smaller markets. BEV registrations fell in only 6 countries on February 2024 levels - volumes in France edged down by 2%, Hungary and Lithuania by 7%, whilst only Estonia, Malta and Romania saw double digit falls. As with the US, appetite seems to be weakening for the current short-range PHEVs on the market - they remain stuck on 7.5% market share across the European market for the first 2 months of 2025, whilst battery electric has reached 17%, up from 12.5%, despite the best efforts of some manufacturers to talk down demand.

Zooming in on the largest markets, Germany hit 18% battery electric market share, a level last reached in the heady days of 2023. Maybe we won’t need to bother with hydrogen fuel cells and e-fuels after all.

France continues to track sideways with 18% market share, as consumer demand is buffeted by reductions in eco-bonuses - the trouble with short-term incentives is that they’re short term. The better news is that petrol and diesel’s tumble continues, hitting a fresh combined low of 31%, down from 41% just 12 months ago, and shows no sign of decelerating. Mild and full hybrids are no long term solution but the new cars the high-income countries of the EU buy today are the used cars the middle and low-income countries will be driving tomorrow, so the trend could be worse.

Outside the EU and with its own decarbonisation standards, battery electric took 26% market share in the United Kingdom in February, the 7th month in a row it has been above 20%, and the second time it has exceeded 25% in 3 months. When CO2 scheme flexibilities are taken into account, industry has already reached its 2025 targets in the year to date. For the UK Government to dilute requirements now following its December consultation would be crazy, and the longer it goes on silently conferring with itself, the crazier the idea looks.

Amongst the high income traditionally lagging countries, Italy reached 5% battery electric market share for the fourth month in a row, the first time it has achieved that run since late 2021. Meanwhile Spain has reached 6% or more for the fourth consecutive month, its best ever result. Both countries are also seeing a gradual squeeze on pure petrol and diesel cars, with plugless hybrids the main beneficiaries. Italy is further ahead with just 36% ICE market share, but Spain is cutting emissions faster, with ICE share down from 56% to 45% in just 1 year.

Now that EVs have a growing toehold in these countries, we can hope to see the EU’s only-slightly-loosened tightening emissions regulation begin to do its work and drive sales upwards. All we need is for the Commission to hold its nerve and Parliament not to cave to manufacturer tales of woe. Giving in will hurt the automotive sector more in the long run.

Top manufacturers

Amongst the top makers across the UK, Germany, Italy, Spain and 4 smaller economies, the continuing story is the decline of Tesla. Whilst registrations bounced back sharply in the UK’s right hand drive market, sales elsewhere were dismal, with registrations falling by 40 to 45% in Spain, Portugal, Italy and Sweden (in line with Europe as a whole, according to ACEA data), 55% in Finland and 70% in Germany. It’s hard to see the cause of the differential performance in Germany as anything other than CEO political interventions - about which the kindest thing one could say is that it might indicate a high level of exposure to the Dumbarse Mind Virus.

Last month we said that this month we would have slightly more idea of whether this is a blip. It’s definitely a longish blip. Next month, which will incorporate registrations of the newly refreshed Model Y, will tell us whether the strength of the product offering - that, and the Trump car dealership operating on the White House lawn - is doing the business.

Still, Tesla is second in February and leads by some distance over the past 12 months.

Who are the beneficiaries of Tesla’s downturn?

Comparing the EU markets for which we have data with January and February 2024 reveals the biggest gainers to have been Skoda, Mini, VW and Renault. Most of these do not jump out as the obvious choice of the liberal-minded hipster executive car buyer.

Nor do Opel, Toyota, Citroen and Fiat, the biggest risers on November and December 2024 levels, before things - and people - got really mad.

Maybe this reveals something about the accuracy of the mental images we have of car buyers. They search out cars which offer good value and appeal, not an expression of their individuality or personality type. And when that car is not such good value, or not appealing any more - or both - they don’t buy it.