Global battery electric sales up 6%, petrol and diesel down 10%, as EVs record best ever January

Global EV Tracker: Insights from 40+ markets accounting for 85% of car sales.

This issue of New AutoMotive’s Global EV Tracker covers vehicles registrations in the first month of 2025.

Fuel type overview

January is a month in which Chinese battery electric registrations tend to dip, relative to ICE vehicles. As the world’s largest car market, this can drag down global results.

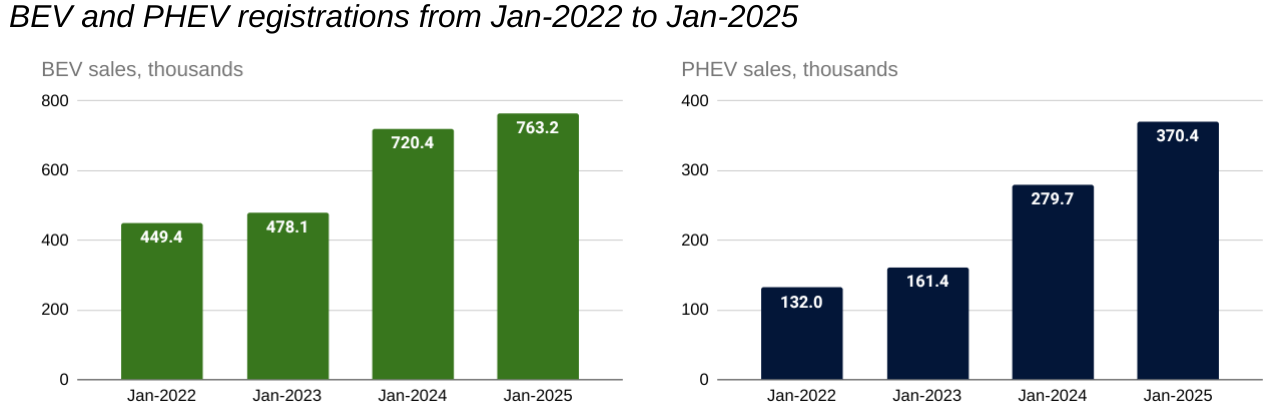

However, battery electric and plug-in hybrid registrations both had their best ever start to the year. Pure electric vehicles reached 763,000 - 43,000 (6%) up on January 2024, whilst plug-in hybrids hit 370,000 - 90,000 (32%) up on the same month last year.

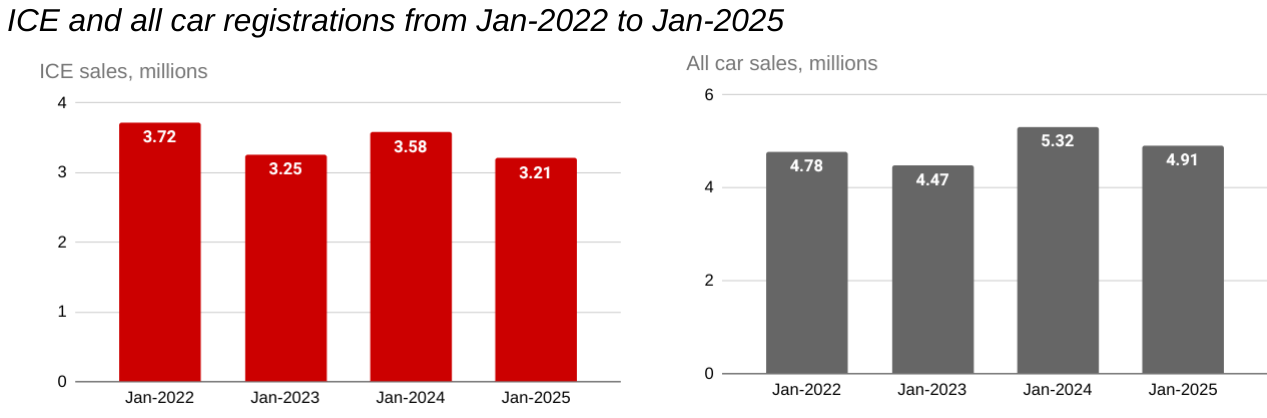

Meanwhile ICE vehicles hit a new post-pandemic low - falling 10% (371,000) to 3.2m.

This sends a strong tailpipe emission-free signal that the switch is set to continue in 2025.

You’re receiving this because you signed up to receive updates from us. Changed your mind? Not a problem, you can change your preferences or opt out of emails here.

The Headlines

In January 2025:

763,000 battery-electric cars were registered, the highest ever January total recorded.

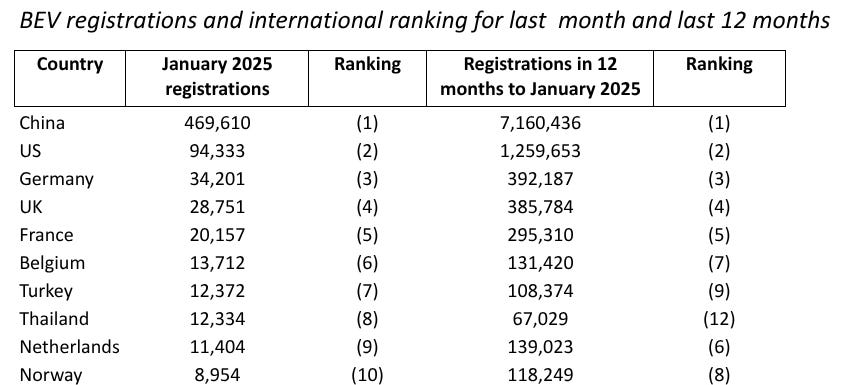

The increases on January 2024 levels were led by the USA (12,000) and Germany (11,750), followed by the UK, with a 7,200 increase. China’s battery electric registrations dipped again slightly by just over 2%, but PHEV volumes surged, increasing by 49% on the same month last year, meaning an overall increase of 83,000 (12.4%) in vehicles with a plug.

Meanwhile, helped by the steep increases above, vehicles with a plug now account for more than 22% of cars - up 16% (3.1 percentage points) on their market share last year.

Don’t forget that for more information, you can check out the Global EV Tracker dashboard - which allows you to produce customised analysis of car sales, market share and manufacturers - at the button below. Our new country profile pages, offering an overview of country-by-country policies and sales, are available at the same link.

Market Indicators

What are the biggest markets for EV registrations?

China and the US are the two largest markets for EVs, as they are for other vehicles. Tesla’s dominance in the US and a continuing squeeze in China (see Asia continent analysis below) makes it uniquely vulnerable to any anti-EV policies introduced by the Trump administration.

Germany, the UK and France come next, followed by 3 other European markets, but Turkey and Thailand’s rise indicates that non-European markets, traditionally dominated by European and Japanese ICE carmakers, are also transitioning rapidly.

Where are we seeing the greatest growth?

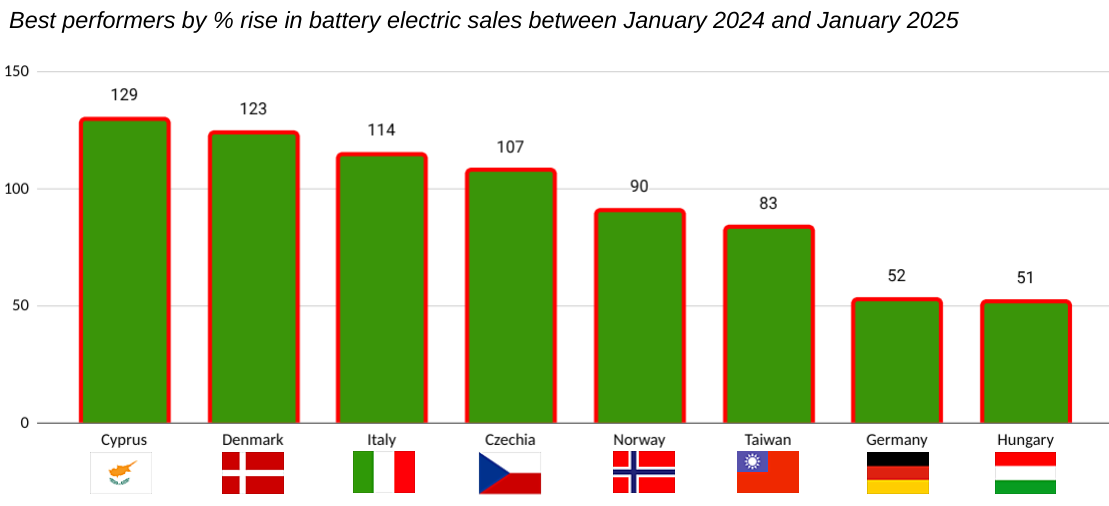

This month 7 of the 8 economies to show the fastest growth were European economies - 6 of them members of the EU. One month into the new, more stretching EU CO2 requirements, this casts some doubt over the assertion by some manufacturers’ representatives that we have a demand problem for zero-emission vehicles (ZEV) in the EU (see Europe continent analysis below). The growth in Germany and Italy, which are together responsible for more than 40% of new car sales in the EU, is especially encouraging.

Taiwan, the only non-European country in the top 8, shows a volatility in registrations which is typical of island nations that rely on imports. However BEV percentage market share there is now into double figures.

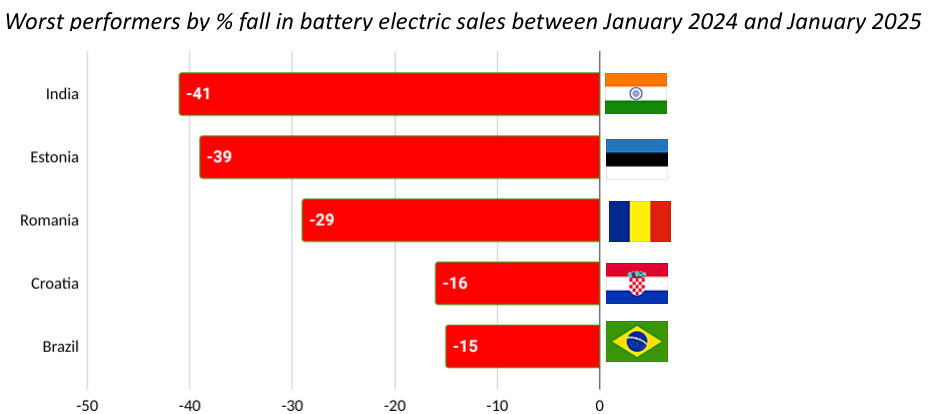

Which markets have been slowest?

The biggest fallers are a mix of small European economies and very large emerging markets. Romania is still coming around from a hangover following the withdrawal of incentives last Spring, whilst Estonia actually had a record-breaking market share of BEVs, albeit in a month with very low sales. These 2 markets, along with Croatia, account for just 2% of car sales, so take up challenges here should be no pretext for weakening regulation.

In contrast the long term fading of India’s 4 wheeler transition remains a concern, even whilst electric 2- and 3—wheeler adoption is soaring. Brazil’s weakening market is also a challenge to some of the very optimistic sales forecasts published in recent weeks (see Americas continent analysis below).

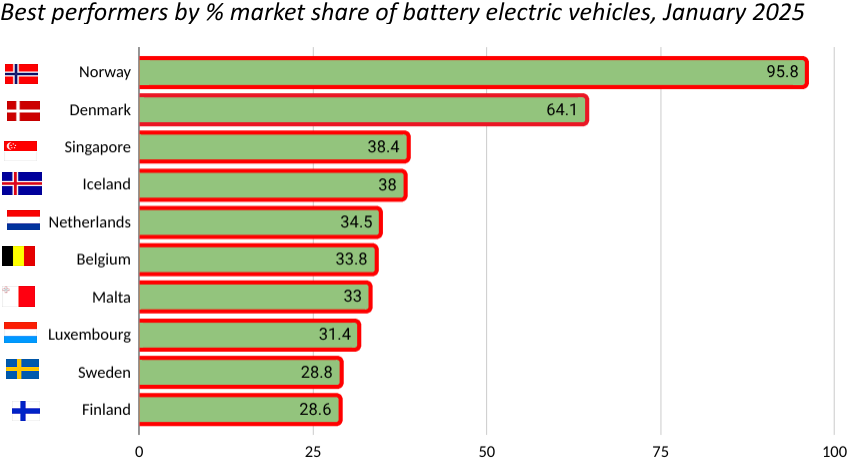

Where is EV market share highest?

The Nordic and Benelux nations hold 8 of the top 10 placings for market share in 2024, whilst Malta has followed a similar approach with broad-based incentive packages. With the exception of Norway, which is set to ban ICE vehicles at the end of the year, all might expect to see further rises in 2025 with new tougher regulations, as long as the Commission holds firm.

Singapore, the only non-Northern European economy in the top 10, has taken a slightly different approach, with rebates for BEVs on otherwise very high vehicle registration fees. That has taken it from 15% to 38% battery electric market share in 2 years, to reach 3rd place this month.

Continent Analysis

Americas

It’s been unclear whether the US market would enjoy one last hurrah for battery electric in January, or whether sales would begin to slide in anticipation of the axe coming down. In the end it plumped for a middle path - BEVs registered 8.5% market share, up from 7.7% in January 2024, with total registrations up 15% over that period. Meanwhile plug-in hybrids accounted for a further 1.9% of the market last month, meaning that market share for vehicles with a plug has been above 10% for 6 of the 7 last months.

Furthermore 3.6 million cars have come onto the road since January 2021, providing a critical mass of demand for infrastructure and servicing. The most that Trump and his allies can really hope to achieve is to slow the switch, not to stop it altogether.

Meanwhile the switch to battery electric flatlined in Brazil. With 3,700 registrations in January and market share above 2% for 13 of the last 14 months, EVs have a toehold, but Bloomberg NEF’s forecast of 59% market share by 2040 is going to need sales to increase by 25% each and every year over the next decade-and-a-half.

It’s a similar story, from an even lower base, in Mexico, where battery electric cars accounted for 1,360 registrations last month, the 6th month in a row that market share has tacked between 1 and 2% market share. The wild policy gyrations of their northern neighbour are going to make any kind of export-led EV transition extremely unpredictable, so harnessing Mexico’s car-making know-how to meet domestic demand looks like a safer bet. On that front, the domestic Olinia, to retail at £3,500-6,000, is a welcome step, but is not set to launch until 2026.

Asia

In China ICE vehicles reached a market share of 62% in January - the highest since March 2024. However legacy manufacturers shouldn’t be getting their hopes up - the previous peaks were January 2023, January 2022, January 2021 … you get the picture. This is a cyclical trend and a slow sales month, and each time sales of vehicles with a plug bounce back faster. 12-month rolling market share of ICE cars reached a fresh all time low of 57%, down from 65% this time last year and down from 84% in 2022.

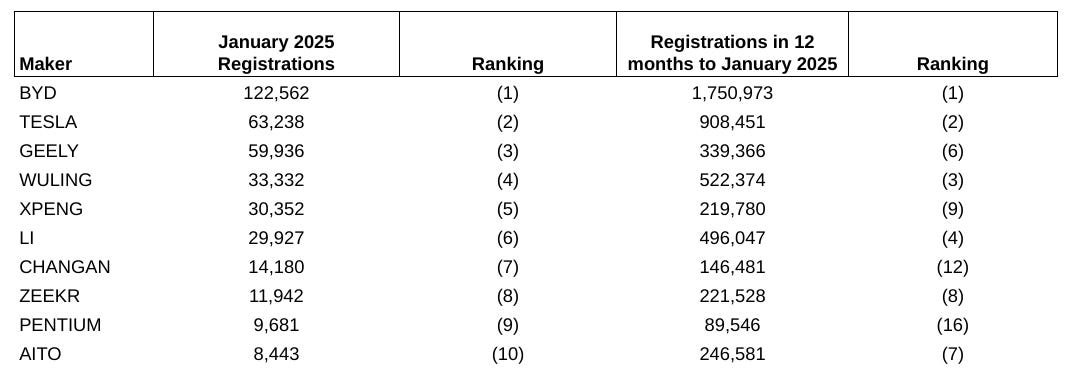

Amongst manufacturers, Geely swiped second place from usual holders Tesla, with sales more than 4 times the level of January 2024, helped by new models such as the Xingyuan. The Tesla crash has yet to materialise in what you might call (don’t tell Trump) its home market, but sales are falling on some measures, with the 3 month rolling average down 5% on the same period last year, whilst the remaining makers in the top 5 - Li, BYD and Wu Ling - rose 12%, 13% and 20% respectively.

Meanwhile other rival makers are moving up fast. Pentium, a joint venture between Hyundai and state-owned BAIC, reached the top 10 for the first time after growing sales by more than 5 times over the last 12 months, whilst BAIC’s own ArcFox brand finished 14th having more than doubled them. That was one place behind Lynk and Co, another Geely brand, which didn’t make a car until September, but registered 7,000 BEVs in January.

Meanwhile BMW were the highest placed European maker in January in 15th place, just ahead of Volkswagen in 17th. BMW sold 100,000 battery electric cars in China in the past 12 months, more than in the 5 biggest European markets put together over the same period, whilst VW sold 167,000.

So the Chinese BEV market remains important, whilst the petrol market is collapsing. All of which makes these makers’ pressure on the EU to weaken regulations so that they can build and sell more cars that they can’t shift elsewhere a tiny bit short-sighted. No other European firms feature in the top 25 EV makers, and Japanese makers have disappeared altogether.

Turning to other Asian markets, Thailand had a great month - across all fuel types, sales were the highest since January 2025, after an extended slump which lasted the whole of 2024. Meanwhile battery electric market share reached 22%, the highest since December 2023 and the second highest of all time. Sales across all fuel types tend to slide seasonally over the year, but battery electric defied the trend and went gangbusters throughout 2023, only to flatline in 2024. We’ll be watching this one closely.

The much smaller Singapore market is also reaching fresh peaks, with a new record of 38% battery electric market share, 55% made by BYD. With sales of 30-40,00 a year, this is a small market, but it’s a sign of how quickly petrol and diesel can fall from favour in cities when they have strong measures on local pollution (in Singapore’s case, through high registration fees). Petrol’s market share has slipped by two-thirds in 2 years, reaching 16% last month, whilst fewer than 4 diesel cars have been registered per month since the beginning of 2024.

Turkey is another market where the public seem to have few difficulties embracing EVs, despite average earnings that are one-third less than the EU’s. Perhaps, being unencumbered by big domestically-owned brands, their big auto sector takes a more practical approach and is less prone to relentless lobbying for the status quo that we see in some jurisdictions. With 12,400 battery electric sales in January, market share was 12%, down slightly on December’s all time high. Nevertheless the trend is sharply upward - with market share growing by more than half on a 12 month rolling average.

Battery electric registrations continue to edge upwards in Taiwan, but it’s a rollercoaster ride. January data saw market share drop to 7%, but this was still enough of a rise on January 2024’s poor figures to mean that the 12 month rolling average market share of BEVs reached 10%, the first time it has hit double digits.

Meanwhile in India, 4-wheelers remain the cinderella of electrification. Despite being committed via the Accelerating to Zero Transition to all new cars being zero emission by 2040, EVs are actually going backward, with 4,000 battery electric sales accounting for less than 1% of sales in January, the lowest market share for 2 years. That said, at 3.5m annual car sales across all fuel types, the market remains relatively small when compared with the US (16m) and China (26m).

Finally to Japan, whose manufacturers and Government have the opportunity to join the dots between the near collapse of Nissan, the absence of Japanese firms from the Chinese EV market (highest placed Honda were 28th) and their high-speed exit from the rest of South East Asia. Not yet though - imports have accounted for 70% of the mere 34,000 battery EVs registered in Japan over the past 12 months, whilst petrol, diesel and plugless hybrid made up 2.5million.

Europe

European battery electric registrations had their best ever start to 2025, across both the EU-27 and the whole of Europe. Across Europe, registrations were up 37% (45,000) on January 2024 levels. A chunk of this is down to Germany, where battery electric volumes rose 12,000 units on the post-crash depths that were plumbed in January 2024, when incentives were unexpectedly withdrawn. But the UK also added more than 7,000 registrations, Norway more than 4,000, and Denmark, Belgium and Italy more than 3,000 apiece on January 2024 levels. In all, 25 markets saw an increase in BEV registrations on the same month last year, whilst only 6 saw a fall, none by more than 400 units.

Zooming in on the largest markets, Germany’s long slow recovery continued. Generally every month’s results are the best since December 2023, the last month that incentives were available, and this month was no exception - battery electric market share is now back up to 17%.

France continues to move sideways with market share of 17%. Plugless hybrids are making more of the running here, leading to the combined market share of petrol and diesel falling from more than half to less than a third in just 2 years.

Outside the EU and with its own decarbonisation standards, battery electric took 21% market share in the United Kingdom in January, the 6th month in a row it has been above 20%. When CO2 scheme flexibilities are taken into account, industry has already reached its 2025 targets over the past 6 months. Despite the best efforts of certain lagging firms to paint this as a general lack of demand, the issue is a particular lack of good products from those firms.

Italy has had a much better January than the previous, but that’s a dismal comparator, as BEV market share dropped to 2% at the beginning of last year. Battery electric accounted for 5% of registrations for the third month in a row - low, but an improvement on the 4% long-term average they were stuck at through most of 2023 and 2024.

Spain also appears to be finally picking up, with 7% market share in January. BEVs have now outperformed their long term average of 5% for three months in a row.

Finally all time highs for battery electric market share were also reached by Estonia (16%), Luxembourg (31%), Denmark (62%) and of course Norway (96%).

Top manufacturers

Amongst the top makers across the UK, Germany, Italy, Netherlands and 4 smaller economies, the big story is the decline of Tesla, which saw registrations crash in every market for which we have data. The 80% fall on December 2024 levels might be explained by the firm pulling out all the stops that month, in an ultimately unsuccessful effort to beat 2023’s figures. More concerning will be the fact that these are the lowest registrations since October 2022. Is the brand doomed by the reputation of its “otherwise occupied” leader? Next month we will have slightly more idea of whether this is a blip.

The big riser this month has been Kia, which saw sales tick upwards sharply in the UK and the Netherlands on December levels, although they fell by a smaller amount in some other markets. The less dramatic faller was Volvo, but this looks to have nothing to do with tariffs on Chinese-backed firms - registrations have also tailed off in the UK, which has none, with figures hitting lows last seen in February. This, like Kia’s rise, are the signs of a competitive market, when new models trounce the competition for a few months before being supplanted by even better models from elsewhere.

Don’t worry if this feels too exciting. Thankfully a lot of entrenched EU carmakers with the ear of national Governments are on hand to slow everything down and make cars more expensive again.

And on that note, how is the EU’s own beautiful tariffs plan going? See below. Yes, it’s labelled correctly. The EU - with much lower and flatlining penetration by Chinese EVs - began an investigation in October 2023, culminating in tariffs which are now in force. Over that period the main Chinese makers increased market share from 7.8% to 10.9%.

But surely - aside from the collateral damage of exempting all the vehicles which they want to discourage people from buying, whilst hobbling their own domestic manufacturers making cars in China - it would have been worse if they hadn’t introduced those tariffs?

Nope. The UK, with a historically much higher market share for Chinese makers, has imposed no tariffs. In the same period, market share of Chinese firms has fallen from 21.1% to 13.9% - almost the same level as the EU - as everyone selling into the UK raced to meet ZEV mandate targets, squeezing out Chinese players.

The concepts that led to this UK success are called (1) free trade and (2) smart and stable regulation. As the Commission-manufacturer “strategic dialogues” stumble unsteadily onward, we warmly recommend them.