Global BEV market share hits record 16.75% in May

After a year of muted market share growth, the BEV mix in global passenger car registrations is picking up the pace

Good afternoon. After a year of relatively modest growth in BEV market share, 2025 is seeing an uptick in EV sales growth. Much of this comes from China, which is not tearing up its EV mandate or watering down fuel economy standards. Half a world away, incentives and regulations are being thrown on bonfires from sea to shining sea. What are we to make of all of this? Read on and hopefully we can help you make sense of it all.

Welcome to Global EV Tracker from New AutoMotive, a monthly newsletter bringing you a roundup of the latest on EV sales in key automotive markets and analysis of what’s driving these trends. If you want to dig into any of the data mentioned in this bulletin, click the button below.

The Headlines - May 2025

11.5m battery electric cars were registered across tracked markets in the 12 months to the end of May - that’s the highest figure ever recorded and 8.5% higher than last year.

1.03 million battery electric cars were registered in May 2025, an 18% increase on May last year, which is roughly in line with the growth in EV sales across 2025 to date.

The rise was largely driven by strong EV sales in China, where EV sales are growing at 21%.

Across the 45+ markets we track, which collectively account for over 80% of the global market for new passenger cars, BEV registrations grew to their highest market share ever recorded of 16.75%.

The market share for BEVs is one percentage point higher than it was this time last year. That might not sound like much, but it represents a significant uptick in the growth in global BEV market share, following a comparatively slower 2024.

Market Indicators

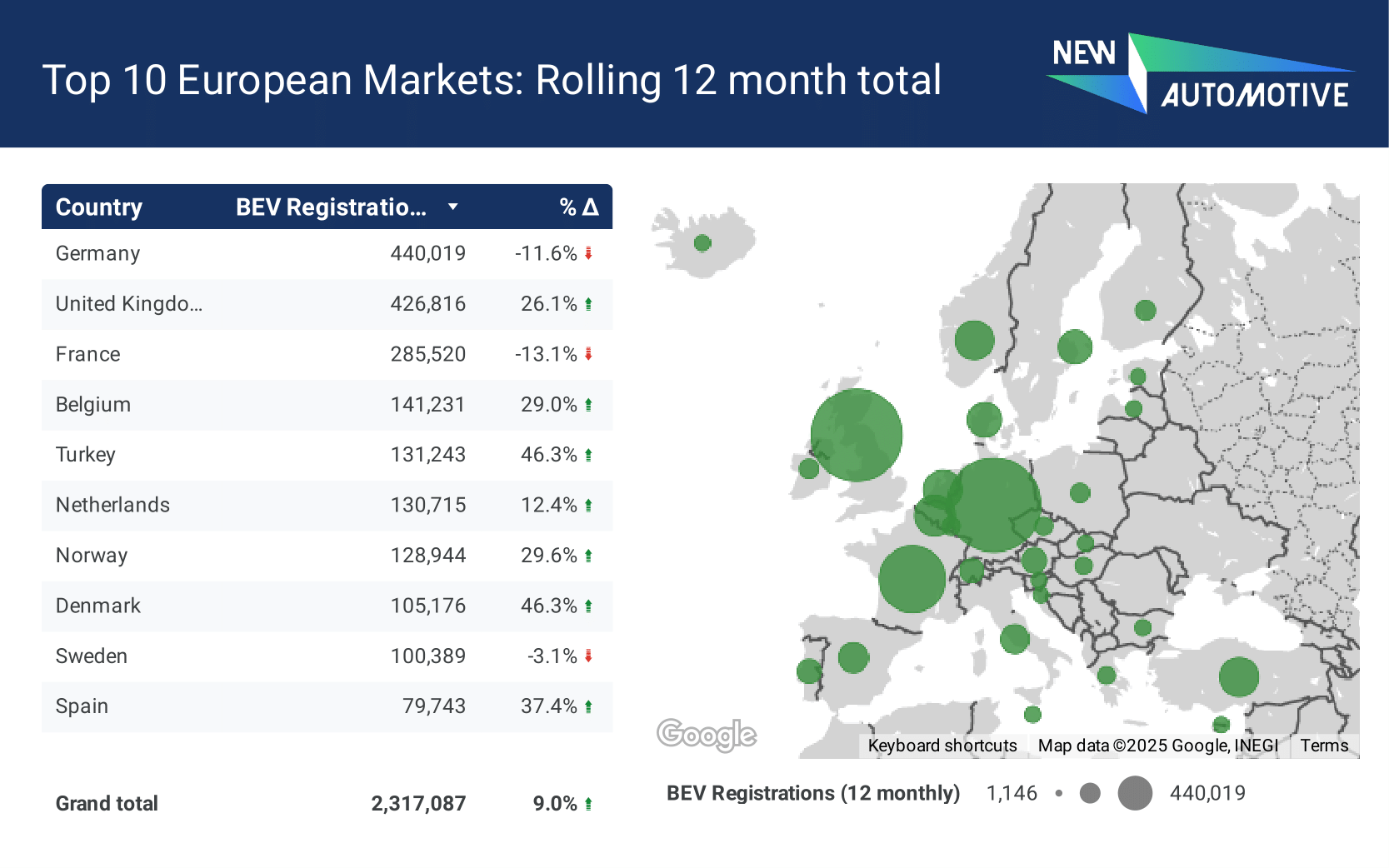

China and the US - for now - continue to be the two largest markets for electric cars. China significantly dominates, with two out of three electric cars registered in the last 12 months bought in China. The rest are European markets, among which there has been some movement over the last few months. One of the big stories of 2025 has been the growth in EV sales in Turkey, where battery electric car registrations have grown 46% in 2025 making it a bigger market for electric cars than Norway.

While many of the fastest growing markets are small or in the early stages of their EV transition - for example, Czechia, Greece, Malta, Brazil, and Cyprus - this table notably includes some markets that are advanced such as Denmark. Growth in BEV sales does not necessarily have to cool off as they become more established in the markets, and the S curve with which we are most familiar might contain a few kinks in it. This likely reflects the sensitivity of BEV market share to the framework of public policy in which the transition is taking place, which can significantly accelerate or restrain BEV sales growth.

Norway continues its unparalleled dominance of the BEV market share ranking, with north of 90% of new cars in the country being BEVs in the last 12 months. If we consider the really significantly large automotive markets, China is the frontrunner with 28% BEV market share in the last 12 months, followed by the United Kingdom with its ZEV mandate-driven impressive 22% well ahead of European peers France (17%) and Germany (16%).

Continent Analysis

Americas

It is too early for policy shenanigans in the United States to show up in these data. The shaking kaleidoscope of legal challenges, Congressional moves to strike down state policy and budget cuts to clean tax credits will be anathema to potential investors in clean vehicle manufacturing, and will significantly raise the financial bar to accessing EVs and their associated running cost benefits. But these will not impact on sales overnight. That said, EV market share has dimmed somewhat in the US and the prospect of EVs getting beyond 10% of the market now looks like it may be significantly farther in the future.

Battery EVs ticked upwards in Mexico, with market share reaching 1.47%, amid an overall contraction in the car market. The future looks significantly brighter for EVs south of the Rio Grande with a major investment summit in Nuevo Leon in June, and various announcements from Mexico City to promote electric public transport.

Further south, Brazil’s EV market continues to grow, with BEV sales taking 3.35% of new registrations in May. This comes as BYD’s largest car carrier vessel arrived in the country in May with a consignment of 7,300 new electric cars, just ahead of tariff increases that threaten to restrict the country’s access to cheaper product markets. Brazil implemented a progressively rising tariff on imported EVs and the level, currently 18%, is set to rise to 25% in July.

Asia

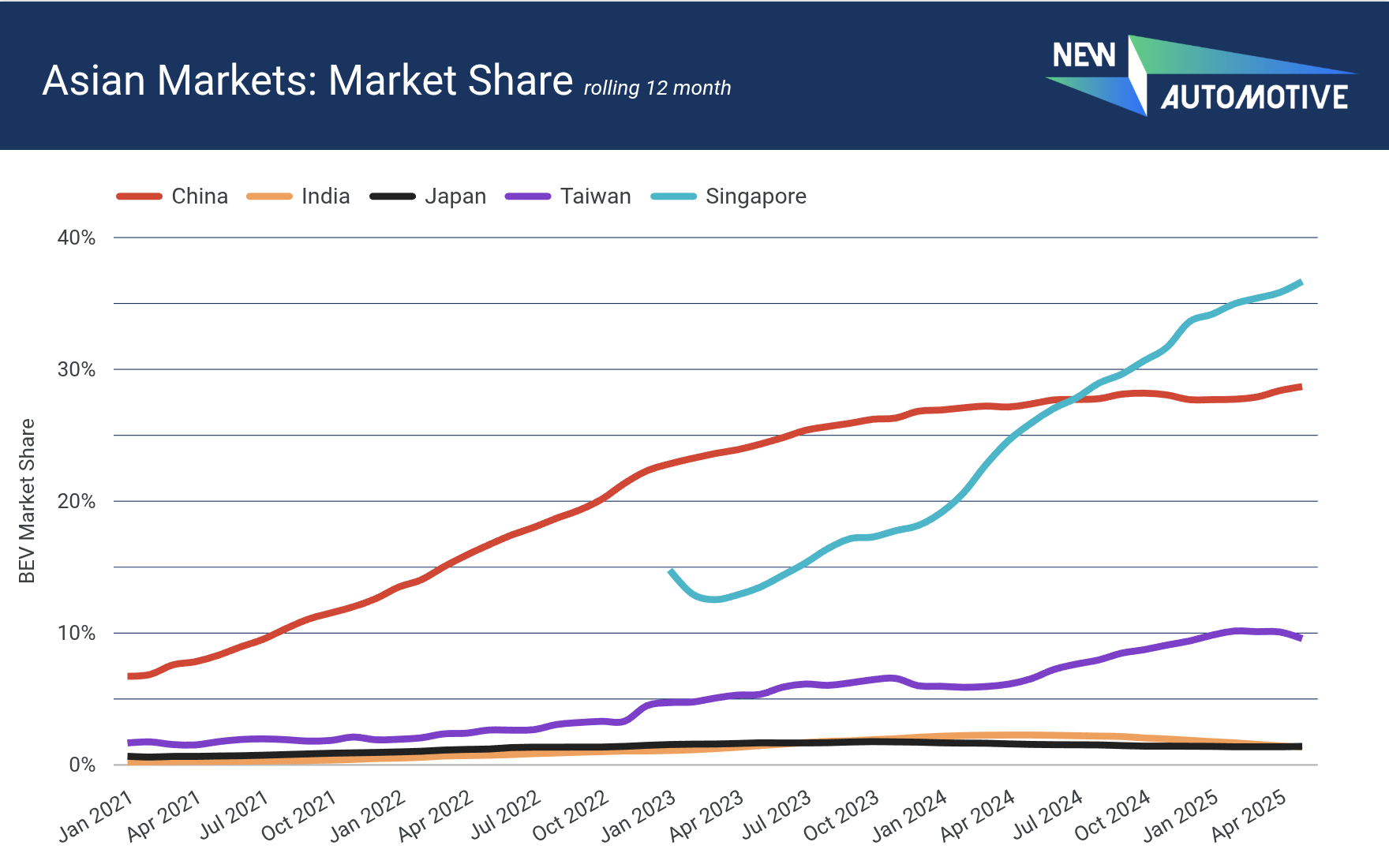

May saw a second all-time high for the market share of battery electric in China, reaching 33% - exactly one-in-three - equalling the market share achieved in April. Registration volumes were 703,000 up an amazing 22.6% on the same month last year. PHEVs saw volumes increase by a more modest 11% to 305,000, meaning cars with a plug accounted for just over 47% of newly registered cars in the world’s largest car market. The ICE share of newly registered cars in the country is in steady and permanent decline. In the last 12 months, ICE cars in China accounted for 55% of all new cars, shedding 7.2 percentage points on the 12 months prior to that.

In Singapore battery electric market share edged upwards to account for 42% of registrations in April, up from 35% in the same month last year. Petrol cars continue to decline rapidly, shedding 8 percentage points of market share over the last 12 months. With new diesel registrations already banned, it is up to policy makers whether to bring forward a ban on other petrol-engined cars from the current target of 2040.

In Taiwan, by contrast, the car industry continues to contract amid concerns over tariffs and a significant fall in consumer spending. Sales of all cars were down 25% in May compared with May 2024, and over the last 12 months overall car sales are down 10%. BEVs have seen a 33% rise in sales volumes in the same period, defying that trend and offering Taiwan’s car market a glimmer of light at the end of the tunnel.

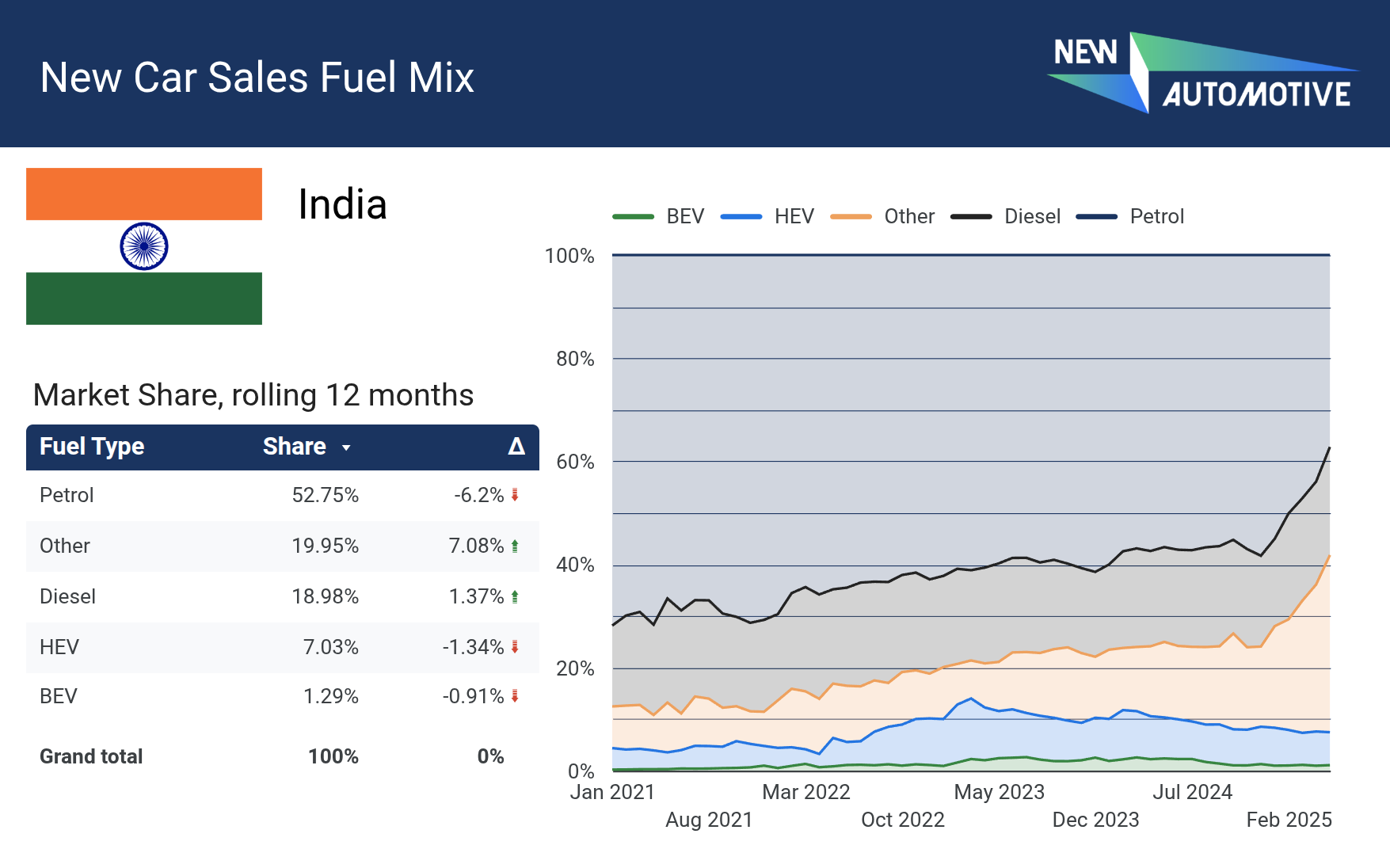

India continues its unique and experimental diversion away from the global electrification trend into alternative combustion fuels. Amongst 4-wheelers, fuels such as compressed natural gas and liquid petroleum gas accounted for 20% of car registrations in the last 12 months, possibly the highest in any major economy. A reminder - India committed at COP26 to 100% zero emission vehicle sales by 2040. BEV market share is down 0.9 percentage points, with BEVs accounting for 1.3% of new cars. Car electrification looks to be grinding to a halt in this large and growing car market.

In Japan, the car market grapples with fuel type stasis, with hybrids accounting for 55-60% petrol for 30-35%, and diesel at 5%, with plug-ins and battery electric accounting for 3% in total. The growth of hybrids appears to have stalled, raising a question for how the Japanese government will continue to find emissions reductions from road transport. Japan’s Top Runner fuel economy programme, in which its vehicle emissions standards are located, contains an unambitious flat target.

Europe

European BEV sales are growing in most markets in Europe, in some places very significantly. As governments unwind subsidy schemes, sales dip. That places more emphasis on supply regulations such as the EU’s CO2 standards for passenger cars and the United Kingdom’s zero emissions vehicle mandate.

Germany’s rolling 12 month total shows a contraction in BEV sales — the product of a car market that has been struggling to find growth amid a stagnant economy and higher interest rates and the unwinding of the Umweltbonus. Yet May itself held much more positive news, with a 44% growth in EVs (and 24% drop in sales of petrol cars). Much of the growth across Europe comes from growing BEV sales from Volkswagen (see below).

In France, the sideways drift of battery EVs continues, meanwhile incentives are reduced, and (sensibly) targeted at households on lower incomes and (less sensibly) subject to an “environmental score”, which is a protectionist measure masquerading as a climate policy. It is certainly not the latter, and will only delay French emissions reductions and act as a drag on Europe’s EV transition, doing little to support France’s already rapidly growing battery manufacturing sector.

As for the EU as a whole, with a BEV market share of 14.3%, Europe is now firmly behind the global average for passenger BEV car registrations. That is not a great look for the European Commission as it faces yet more pressure from carmakers to abandon its 2035 goal to end sales of petrol and diesel cars.

In Turkey battery electric cars continue to grow very strongly, taking 18% of the market in May, rising from under 10% a year ago. Petrol car registrations are entering a nosedive, driven out by hybrids and battery electric registrations growing at 97% and 47% respectively over the last 12 months. This rapid progress is being driven in large part by Togg, the country’s new electric car brand, who have rapidly become the market leader with their T10 starting at 1.4m TL (£26,400 or US $36,200).

Belgium continues to see particularly rapid growth in EV sales, on the back of a highly progressive company car taxation system. This approach - in which corporate fleets are incentivised to choose battery electric - has proven highly successful in many markets, and often provides a much better approach than obligations on corporate fleets which run the risk of producing perverse outcomes.

Outside the EU and with its own decarbonisation standards, battery electric took 22% market share in the United Kingdom in April, with overall EV sales growing by 22%. With the expanded flexibilities announced but not yet introduced by the UK Government, it looks as if manufacturers are within 2 percentage points of meeting the 2025 Zero Emissions Vehicle target. They were considerably further away from the 2024 target at the same point last year and nevertheless comfortably exceeded it.

Top manufacturers

In Europe, Volkswagen group brands have made significant progress on their EV sales, following a brief dip towards the end of 2024. Growth of 30.4% in the 12 months to the end of May is significant. Also of note is Ford’s entry into this top ten ranking, which comes off the back of explosive BEV sales growth in many European markets.

Tesla’s sales patterns are well-covered, but their 12 monthly sales in these selected European markets is notable for its 12% fall. The once market leader looks increasingly vulnerable to some of the incumbent European OEMs.

China’s EV market is so huge that it is worth looking at the manufacturer breakdown in isolation. BYD continues to exhibit remarkable sales growth. But perhaps one of the most striking things that we observe is how many manufacturers are present and thriving in this market, which is being driven by an ambitious ZEV mandate system in the form of China’s dual credit policy and fuel economy standards - precisely the policies that Europe and America are in the process of watering down.

With that, we bid you a good month, see you next time!

Global EV Tracker monitors passenger car registrations from 40+ markets representing over 80% of global car registrations, updated monthly. The countries we covered in this bulletin are: China, United States, India, Germany, Japan, Brazil, United Kingdom, France, Mexico, Italy, Spain, Turkey, Poland, Belgium, Taiwan, Netherlands, Sweden, Austria, Portugal, Czechia, Switzerland, Denmark, New Zealand, Norway, Greece, Romania, Hungary, Ireland, Slovakia, Finland, Croatia, Slovenia, Singapore, Luxembourg, Bulgaria, Lithuania, Estonia, Latvia, Cyprus, Iceland, and Malta.