No triumph, no tragedy. Plug-ins now account for 30% of registrations. And maybe people don't mind Tesla after all.

Global EV Tracker: Insights from 40+ markets accounting for 85% of car sales.

This issue of New AutoMotive’s Global EV Tracker covers car registrations up to the end of March 2025. We hope you enjoy our take on the latest moves in EV registrations around the globe. Don’t forget that you can always dig through the numbers yourself….

Fuel type overview

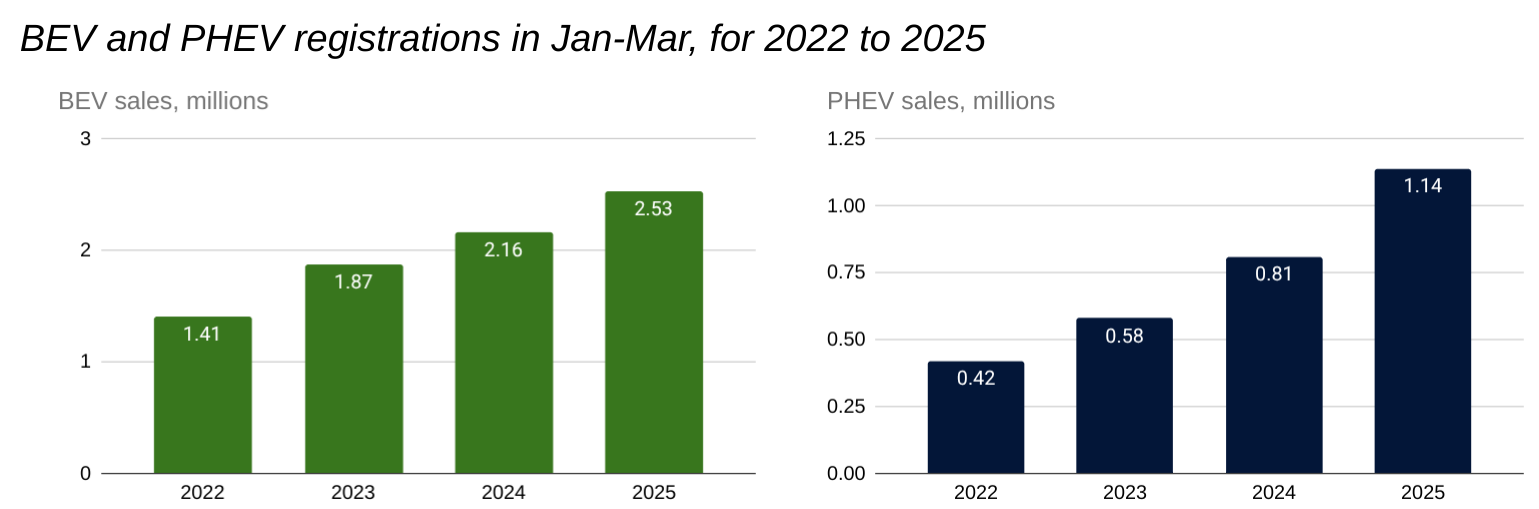

The switch is still happening day-by-day, month-by-month. Pure electric car registrations reached 2.5m in the first three months of the year - 370,000 (17%) up on Q1 of 2024, whilst plug-in hybrids hit 1.1m - 330,000 (41%) up on the same time last year.

Meanwhile ICE cars are down again. As with last month it was only rising BEV and PHEV registrations which meant that car sales increased at all.

Slowly slowly, the silent electric woodsnake catchy the noisy belching ICE monkey.

You’re receiving this because you signed up to receive updates from us. Changed your mind? Not a problem, you can change your preferences or opt out of emails here.

The Headlines

In March 2025:

1.04 million battery-electric cars were registered, the highest March total ever recorded and a 152,000 (17%) rise on the same month in 2024.

The rise was as ever led by China, the world’s largest car market, with an increase of 88,000 EVs on last March; the UK, with 19,000 additional sales in its best ever month; the USA, defying climate denialism with 18,500; and Germany with 11,000 extra registrations. Smaller rises in Turkey, Spain, Italy, Thailand, Denmark and Norway make up the rest of the increase.

Tesla sales bounced back strongly in China, re-taking 2nd place behind BYD; and in Europe, where they beat all other carmakers in March.

Globally, cars with a plug now account for 30.0% of registrations in March - up 15% (3.8 percentage points) on their market share last year. Call this flatlining?

Don’t forget that for more information, you can check out the Global EV Tracker dashboard - which allows you to produce customised analysis of car sales, market share and manufacturers - at the button below. Our new country profile pages, offering an overview of country-by-country policies and sales, are available at the same link.

Market Indicators

What are the biggest markets for EV registrations?

China and the US are the two largest markets for EVs, as they are for other fuel types. The UK’s strongly seasonal market, driven by new number plates in March and September, saw it take third place this month, but an exceptionally strong market this year has seen it overtake a rebounding Germany over the past 12 months too.

A strong run has continued for the third largest non-European EV market, Turkey, overtaking the Netherlands this month and is close to catching seizing Norway’s 8th place, when measured over a 12 month period.

Where are we seeing the greatest growth?

Whilst some small markets periodically enter the top 10 as a result of short term blips in EV sales, Czechia and Denmark have been amongst the top risers for 3 months in a row, and Spain, Italy, Iceland and Slovakia for two of the last three months. Denmark is an exception in continuing to grow rapidly despite already having one of the highest market shares of EVs. Iceland’s boom is more of a comeback from an ill-conceived road-pricing scheme which crashed EV registrations at the beginning of 2024. The sustained momentum of Czechia, Slovakia and the much larger Spanish and Italian markets, shows that there is nothing pre-ordained in the take up of EVs. With strong policies and stable incentives, the switch can pick up pace anywhere. Although Ministers dialling down their anti-EV rhetoric has also helped in some of these markets.

Where is EV market share highest?

The leading markets are also remarkably consistent, from month to month. Only Malta has fallen out of the top 10 in 2025. In March, Iceland and Finland edged ahead of Singapore, but the other positions are unchanged on February.

The Nordic and Benelux nations hold 8 of the top 10 placings for market share in 2024. With the exception of Norway, which is set to ban ICE cars at the end of the year, all might expect to see continued further rises in 2025 with new tougher regulations coming into force, even with a recently proposed 3 -year averaging period - although manufacturers may be more likely to target Italy and Spain (see Europe Continent Analysis below).

Of the two Asian markets in the top 10, Singapore’s market is only slightly larger than Luxembourg’s, but China in 10th, buys more EVs than the rest of the world put together and sales are rising steeply (see Asia continent analysis below).

Continent Analysis

Americas

March was an exceptional month for the USA. With on-again-off-again tariffs on imports from Mexico and Canada, a cranking up of taxes on Chinese imports and a 25% auto tariff announced on the 26th, manufacturers, dealers and buyers boosted registrations in a traditionally busy month to a huge spike of 1.59m, the highest level for 4 years. Battery EVs and PHEVs both benefited from this surge, but less than traditional ICE vehicles, resulting in market share sliding downwards a little 7.3% and 2.4% respectively. Overall battery EV sales have held up well in the first 5 months of reported registrations since Trump’s election victory, with more than half a million coming onto the road. Every month looks like it’s going to be exceptional for the USA one way or another this year, but the clock isn’t turning back on the switch to electrified transport.

Turning to Brazil, battery EV sales crept up to 2.7% in March, a 10-month high. When plug-in hybrids are considered, market share has been above 6% for the whole of 2025 to date, and Q1 registrations are up 23% on the same period last year.

After rapid growth in 2024, Chile also looks to be slowing. EVs reached 2.2% market share in March, the best result for 2025, whilst Q1 registrations are up 150% on the same period in 2024. So far, so good. But market share growth has slowed in since early Autumn. With only a small amount of domestic car production, Chile bears little risk from the lobbying of local incumbent carmakers, and could useful begin work on a supplier mandate which encourages manufacturers to bring forward competitively-priced EVs that work for everyone.

Battery EVs also scored their best month of the year to date in Mexico, but this too is a low bar - it took 1,650 registrations and 1.3% market share to set a record for 2025. Even hybrids aren’t making inroads here - market share of ICE cars remains at 90%. As we said pre-tariffmageddon, Mexico’s best bet to put its large motor manufacturing industry onto a surer path to electrification might well be to boost domestic demand with supply-side measures of the type used in Europe and China, and use its lower domestic labour costs to favour local manufacturers.

Asia

March is always a strong month for registrations in China, after a traditionally quiet old-year-end and new-year-beginning. So sales of all fuel types were up, but battery electric had the best outcome, with 640,000 registrations accounting for 29% market share, the highest since September 2024. PHEV market share unexpectedly fell slightly to 14%, meaning that the proportion of ICE registrations held steady at 58%. However this is still down from 63% in March 2024. We expect vehicles with a plug to account for more than half of registrations soon - if not by late 2025, then in early 2026.

Tesla registrations in China rebounded sharply last month, with registrations up 150% on February levels. Whether this is a blip as deliveries of the refreshed Model Y hit the streets and the tariffs play out - or whether January and February’s slump was a blip - remains to be seen. Wuling (44% owned by General Motors) and Geely’s own brand vehicles complete the top 4, as they did last month, whilst Geely-owned Zeekr is also in the top 10. XPENG, who only scraped into the top 10 last year, are now up to 7th over the past 12 months and reeling in state-owned Aion.

Outside the top 14, VW - who also own a slice of XPENG - had a surprisingly strong month, with 8,500 registrations and a 14th place, with Toyota and BMW also up to 15th and 16th. Perhaps there is still hope for European and Japanese makers in the world’s biggest car market after all.

Turning to other Asian markets, Thailand saw a rebound with battery electric accounting for 17% of car registrations in March and a similar proportion over the first 3 months of 2025 - its best ever start to a year, and up 32% on the same period in 2024. Thailand is unusual in having battery EV manufacturing targets rather than sales targets, but home demand will provide some security and confidence to policymakers and automakers alike as we enter the tariff maelstrom.

The Singapore market saw battery electric cars account for 39% of registrations in March. The three month rolling average is now above 40% for the first time. BYD long ago took over leadership of this market, with 49% battery electric market share this month, whilst Tesla (9.0%) and BMW (8.6%) are second and third. Meanwhile XPENG - surging in China, growing in the EU and now entering the UK market, were 4th in Singapore for the first time in 6 months, reaching 5.7% market share. Whilst diesel is now at less than 0.5% and petrol is down to 17%, these figures are unchanged on last March. So battery electric’s cannibalisation of hybrid car demand continues, with market share of the latter down by 12% in 12 months.

Meanwhile Turkey recorded a battery electric market share of above 10% for the 7th time in a row - reaching 13% last month, well up on the 8% achieved in March 2024. But the main story, in contrast to Singapore, is the continuing collapse in petrol and diesel car sales as these are replaced by plugless hybrids. Market share for “pure” ICE cars last month was 57%, down by more than one-quarter on the 78% chalked up in March 2024. Meanwhile hybrid registrations more than doubled their share to hit 31% in the same period. We shouldn’t need to wait for petrol and diesel to be wiped out by a petrol engine with a 1kwh battery before real EVs make a bigger breakthrough, but that seems to be what we are witnessing in the Turkish market.

In Taiwan, BEVs and hybrids are more equal beneficiaries of the switch from petrol and diesel. Cars with no battery driving the wheels have steadily declined from 70% market share in March 2023, to 63% in March 2024 and 57% last month. Like Turkey, they are set to dip below 50% imminently. Whilst plugless hybrid take-up is responsible for a bit more than half of that decline, battery electric is getting the rest, and in the past year has grown from 6% market share on a 12 month rolling average basis to 10% last month, the first time it has reached this level. On a month-by-month basis BEV registrations edged up marginally to 8.5% in a market which regularly yo-yos.

India’s retreat from battery electric 4-wheelers continues despite ever more wildly optimistic statements from its Transport Minister. If India is to overtake China as an EV manufacturer in 5 years, it would be helpful to have a plan for increasing the volume of domestic buyers from the current 1% to China’s current 30% (which is very likely to be at least 50% by 2030). Instead, dead-end alternative combustion fuels are the only growth sector, and set to overtake diesel, with both recording 21% market share in March. With petrol accounting for 47% of March volumes, 89% of the cars flowing into some of the most polluted cities on earth can only burn stuff. It’s not big and it’s definitely not clever.

Whilst the car-makers of Japan are facing up to international economic realities and bringing forward new battery EVs, the domestic market remains in the deep freeze. 4,000 EVs were registered in March, the best result since November 2023, but in a strong month for car sales, BEV market share was still only 1.4%. Nissan leads the Japanese battery EV makers, outselling Toyota by 7-to-1. But the domestic offering is so weak, 82% of battery electric car registrations were imported. Even plug-in hybrids, which Japanese makers were amongst the first to bring to market, are stuck at 1.7%, whilst the decline of petrol and diesel also appears to have paused, levelling off at 37-38% market share.

Europe

Despite the best efforts of trade bodies to present the data as a boom for hybrids whilst battery electric disappoints, battery EV is the fastest growing fuel-type in the year to date, rising 24% across the EU and 28% across Europe as a whole on the same period in 2024.

Battery electric share is now 15.2%, up by more than a quarter, whilst PHEVs make up 8% and hybrids 36% in the year to date. Meanwhile petrol and diesel are down by a fifth (to 29%) and a quarter (to 10%) respectively. All of these transitions contribute to meeting targets in the EU’s emission-based regulation.

Other things you will not read in an ACEA press release are that battery electric registrations rose in 21 markets and only fell in 6, whilst petrol sales fell in 23 of 27. The only large markets to see a decline in BEV registrations were France - where battery electric is still inching up slowly, from 17.9% to 18.0% in the year to date; and the Netherlands - where it is surging, from 30% to 35% over the same period. Traditional petrol and diesel cars are dead men walking in both markets - down by a third in each over a 12 month period, to fresh all time lows of 26% in France and 14% in the Netherlands last month.

The long march of Germany back from a collapse in demand following the chaotic withdrawal of incentives at the end of 2023 continues. Market share is now up to 16.9% in quarter 1, a 45% rise on the 11.7% achieved in the same period of 2024. Germany is now the only one of the large European economies where petrol and diesel account for more than 40% of vehicle registrations, but it’s beginning to fall fast here too, with a decline of a fifth since Q1 of 2024 to reach 45% in the year to date.

Meanwhile, assisted by EU policy, sales are finally taking off decisively in the historic lagging markets of Spain (from 4.4% in Q1 2024 to 6.4% in 2025) and Italy (from 2.9% to 4.9%). As large and prosperous countries with an untapped early adopter audience, we expect these two to receive a lot of attention from manufacturer marketing teams in the coming months as firms compete to hit their average CO2 targets. As long, that is, as the Commission rejects the siren voices of some in the industry and Parliament luring them onto the rocks of illusory e-fuels and ethereal offsets.

Finally plug-in hybrids, which manufacturers are lobbying to keep selling after 2035, are being left behind by a battery EVs, with a smaller and slower-growing market share and a rise of just 0.2 percentage points to 7.6% in the first quarter of 2025.

Outside the EU and with its own decarbonisation standards, battery electric took 20.8% market share in the United Kingdom over Q1, up from 15.5% on the same quarter last year. When flexibilities were taken into account the industry was within a whisker of meeting its targets, and now that Government has diluted regulations to appease domestic manufacturers such as, er, Nissan, Toyota and Tata Group, it it now awash with credits, and compliance for all will be very low cost . Naturally this isn’t enough for some manufacturers who want to go back to selling battery electric cars at a 50% premium, or perhaps not having to get around to selling any at all. The UK Government must recognise the high skill jobs in charging, infrastructure and generation which are at stake in the transition and tell the cartel to do one.

Top manufacturers

For the markets where we have carmaker data (the UK, Germany, Italy, Spain, the Netherlands and 4 smaller economies), Tesla sales bounced back as they did in China, increasing by more than 100% on February’s suppressed levels. Tesla sales are still down on their long term average, leading VW by just 5% in March, rather than the 30% seen over the past 12 months. However the refreshed Model Y only began to ship during March, so we could see a further steep rise in April and a reversion to pre-DOGE levels. Talk of long-term brand damage could still prove overstated - the real problem remains an increasingly tired and limited product range lacking any budget options.

Kia’s strong performance continues, as they overtake parent Hyundai. BYD has its first month amongst the top 10 makers after steadily improving sales, although two-thirds of its March registrations relate to a right hand drive shipment for the UK, so we do not expect to see it appear regularly in the top 10 for a while yet. For now, and for all the scaremongering, European makers are dominant, with VW Group accounting for almost twice Tesla’s registrations when the Audi and Skoda marques are included.

For all the rollercoaster ride of tariffs, it looks like the transition is panning out in a way which is less exciting and more sedate than we might have expected. No firms are crashing and burning, although some - especially several Japanese makers - are already into a long, slow downturn. Many or most others will survive the switch, and rise to the challenge from Chinese firms. It won’t stop them complaining, of course - and for the firms that do survive, it will of course be their strategic brilliance, rather than good regulation and consistent policy, that saved them.

There won’t be any statues for the policymakers that make this happen. But no-one will remember the names of the carmakers’ trade body executives either.