Not braking, but bouncing

Global EV Tracker: Insights from 40 markets accounting for 85% of car sales.

This issue of New AutoMotive’s Global EV Tracker covers car registrations up to the end of April 2025. We hope you enjoy our take on the latest moves in EV registrations around the globe. Don’t forget that you can always dig through the numbers yourself….

Fuel type overview

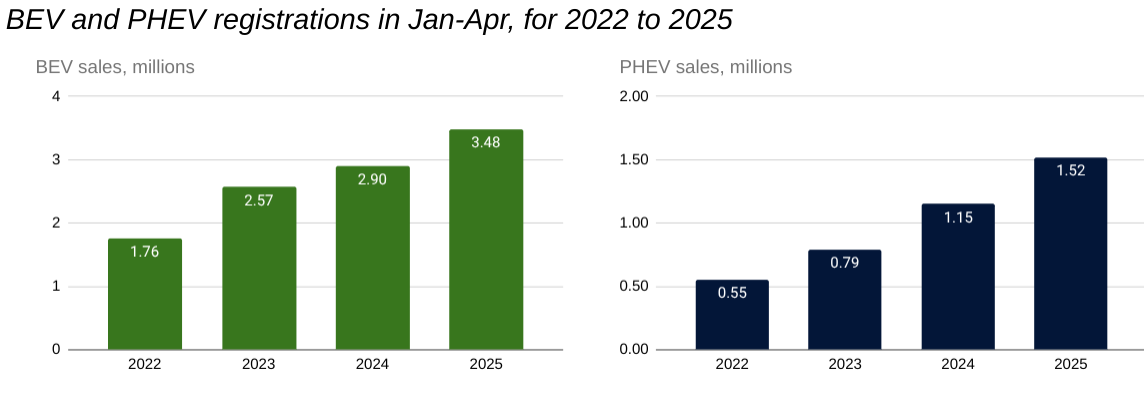

Battery EV registrations are up 20% (580,000 to 3.48 million) in the first 4 months of 2025 on the same period in 2024, an acceleration on last year’s rise of 13%. So battery electric sales are not slowing they’re speeding up. Who knew? Apart from our readers of course.

Plug-in hybrids are up 32% (370,000 to 1.52 million)in the year to date, meaning that vehicles with a plug now account for 23% of registrations.

Meanwhile ICE car registrations - which have never regained pre-pandemic volumes - are down a further 4% on last year’s depressed levels. Every month, it’s only the increase in plug-in registrations which mean car sales are rising substantively at all.

Car manufacturers betting on a resurgence of petrol and diesel are ostriches looking for their navels with the wrong end of a telescope.

You’re receiving this because you signed up to receive updates from us. Changed your mind? Not a problem, you can change your preferences or opt out of emails here.

The Headlines

In April 2025:

977,000 battery-electric cars were registered, the highest April total ever recorded and a 218,000 (29%) rise on the same month in 2024.

The rise was as ever led by China, the world’s largest car market, with an increase of almost 181,000 EVs on last April; Germany with nearly 16,000 and Turkey with more than 5,000. Smaller rises in Spain, Belgium, Italy, Denmark and Austria make up the rest of the increase.

After a brief bounceback with the fulfilment of pent up orders of the refreshed Model Y, Tesla has slid again - they’re now down to fourth in China, their largest market, and have fallen out of the top 10 in Europe altogether.

Globally, cars with a plug now account for 24.7% of registrations in April - up 17% (3.6 percentage points) on their market share last year. So - no, not flatlining.

Don’t forget that for more information, you can check out the Global EV Tracker dashboard - which allows you to produce customised analysis of car sales, market share and manufacturers - at the button below. Our new country profile pages, offering an overview of country-by-country policies and sales, are available at the same link.

Market Indicators

What are the biggest markets for EV registrations?

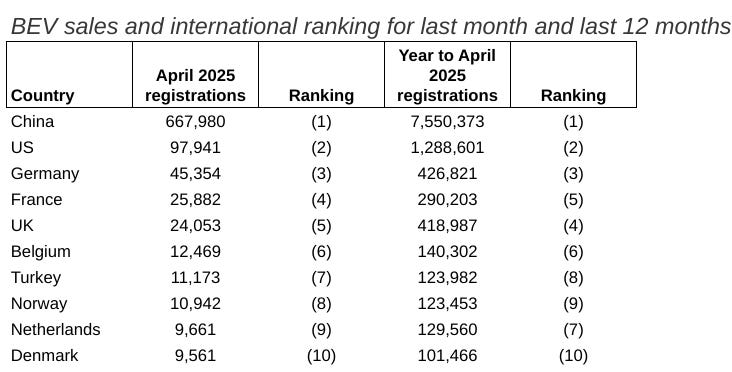

China and the US are the two largest markets for EVs, as they are for other fuel types. Surging growth in the large German market (see Europe continent analysis) has seen it retake third place, but the UK remains well ahead of France in fifth. The main story is Turkey’s continued march (see Asia continent analysis) - overtaking Norway when measured over the past 12 months, with the potential to pull ahead of the Netherlands - a country with almost 5 times the per capita income - in the next few months.

Where are we seeing the greatest growth?

For the first time, all the fastest growing markets are in Europe. Most countries in the top 8 are at a relatively early stage in their journey, with less than 10% battery electric market share. The exceptions are Austria, where battery electric accounted for 23% of registrations in April; and the tiny Icelandic market, which is still restarting its market more than a year after the introduction of a disastrous EV-only road pricing scheme. Battery electric accounted for 24% market share last month.

Of the other countries, it’s worth mentioning Czechia, which after rapid growth from a very low base, is now seeing consistent battery electric market share of 6%; and Poland where, thanks especially to progress in the first few months of 2025, battery electric market share has topped 5% for the first time.

Where is EV market share highest?

A few countries have swapped places in the top 10, but the only change of membership is the return of Malta in place of Luxembourg. Many of the markets in this top 10 are small, so China’s slight rise, from 10th last month to 8th this month, reveals a huge shift in buying habits, China’s increase in battery EV registrations, from March to April, is more than three times the size of the total April registrations of all the other countries in the top 10 put together.

Continent Analysis

Americas

As tariffs began to bite, April looked like another exceptional month for the USA with registrations topping 1.463m, the third highest total in 4 years. Panic-buying, rather than economic bullishness, looks to be the more likely explanation. Battery electric sales continued to hold up whilst the dizzying parade of reviews, cuts, clawbacks and trade wars continue. Market share of battery electric was 6.7% in April, a slight dip on the 7.5% recorded in the same period last year, but registrations in the year to date are still up 12% on 2024 levels, whilst petrol cars are up less than 2%. With a 50% increase, hybrids are the biggest gainers, although with a market share of only 12%, the US’s stumbling journey towards decarbonisation has a lot further to run.

That won’t have been helped by Congress’s removal of California’s waiver to set EV registration targets (almost certain to face legal challenge), or the likely withdrawal of consumer tax credits. Like American football, acidic chocolate and prescription opioids, the US appears to be taking its own solitary turn.

Battery EVs ticked upwards in Mexico, with market share reaching 1.56%, the best result since October 2024. However hybrids are the only fuel types whose registration numbers have increased in the year to date compared with the same period in 2024, increasing by one-third to reach a market share of 7%. Like the US, but unlike European and far Eastern markets, Mexico is coming late to hybrids, with pure ICE cars accounting for 90% of registrations. However we don’t really have the time to go through decades of people getting used to hybrids before switching to battery electric in the middle of the century. With a more pragmatic and less narcissistic leadership than its rivals, Mexico is in a position - if it chooses to - to leapfrog from petrol to plug-ins.

Brazil is already making this move, with most of its hybrids being of the plug-in variety. Vehicles with a plug made up 6.5% of registrations in April, the highest figure since December 2023. Whilst registrations are only up 7% on the same month last year, petrol sales are down more than 10%. There are storm clouds on the horizon however, as domestic makers - champions of free trade when it suits them - call for tariffs to protect themselves from better carmakers such as BYD. If only there were some countries who had tried that and could report on how stunningly unsuccessful it had been.

Chile had its third best ever month of battery electric registrations (by units and by market share) in April (its best was in December), but with BEVs accounting for 512 units and 3.0% of sales there is a way to go. Still, registrations in the year to date are twice what they were in the same 4 months of 2024, so there is a lot to be positive about, and Chile’s relative lack of go-backward-can’t-do car manufacturing incumbents gives it an advantage over its neighbour.

Asia

April saw a fresh all-time high for the market share of battery electric in China, reaching 33% - exactly one-in-three - for the first time. Registration volumes were 668,000, up an amazing 43% on the same month last year. In contrast plug-in hybrid market share was flat at 14%, meaning that vehicles without a plug - including hybrids - held on to just over half of the market. Given the pace of decline, from 60% market share in April 2024 to 53% today, it’s only a matter of months before EVs become the majority choice.

Tesla bounce in March is beginning to look like a blip. This month they were pushed down to fourth place by Wuling (44% owned by General Motors) and Geely (Zeekr, owned by Geely, is also in the top 10). Both firms will need to outsell Musk’s struggling outfit by more than they did this month to take 2nd place from him this year - but the period when Tesla outsold every maker other than BYD by 2 to 1 feels a long time ago now. It’s hard to maintain success when you last launched a new model 5 years ago and your flagship (the refreshed model Y) starts at $36,400 in a furiously competitive market.

Outside the top 10, Volkswagen edges up to 13th, overtaking one-time Huawei-backed AITO. Toyota take 15th, and have the potential to climb with the launch of the bZ5, a Tesla Model Y at half the price.

In Singapore battery electric market share edged upwards to account for 40% of registrations in April, up from 35% in the same month last year. Petrol’s steep decline has levelled off to reach 17% - pretty much the share identified as skeptics or laggards in the adoption curve. With new diesel registrations already banned, it is up to policy makers whether to bring forward a ban on other petrol-engined cars from the current target of 2040. Singapore is already ahead of many countries with more ambitious targets. BYD have 52% of the market, which reflects their ongoing dominance. Amongst those fighting for the crumbs, Tesla were second with 8% market share, state-owned Chinese firm GAC third with 7%, and BMW and XPENG 4th and 5th with 6% and 4% respectively.

In Turkey battery electric cars scored a market share of above 10% for the 8th month in a row - reaching 14% last month, well up on the 9% achieved in April 2024. This performance means Turkey leads amongst the Mediterranean countries in our tracker, and is well ahead of richer near-neighbours such as Spain, Italy, Slovenia, Croatia and Greece. Meanwhile the slow-motion collapse in petrol and diesel continue, with combined market share down from 75% in April 2024 to 54% last month.

In Taiwan, by contrast, BEVs had a relatively poor month, accounting for only 5% of registrations. However monthly registrations of all fuel types are volatile and battery EV registrations in the year to date are still up 17% on the same month last year. Meanwhile hybrid car sales are only up 8%, whilst petrol car sales are down 24% in the same period. As with Turkey, petrol and diesel are on the verge of losing the majority status they have held for more than 100 years.

We forecast that India would soon see its mad adventure into alternative combustion fuels overtake diesel and so it has proved. Amongst 4-wheelers, fuels such as compressed natural gas and liquid petroleum gas now account for a total of 29% of car registrations, possibly the highest in any major economy and more than doubling April 2024’s market share. Petrol is down from 57% to 44% over the same period, whilst diesel holds steady at 20% and hybrids and battery electric go backwards. A reminder - India committed at COP26 to 100% zero emission vehicle sales by 2040. Four years have passed and battery electric sales have increased by 0.3 percentage points. The pace need to increase 90-fold to meet its target.

It’s been a month of contrasts in Japan as Toyota looks to accept electrification, Nissan cuts 20,000 jobs and 7 of 17 plants, whilst Honda continues to burrow an ostrich-head shaped hole in its retreat from electrification . However the domestic market is the same as it ever was, or has been for the past 18 months, with hybrids accounting for 55-60% petrol for 30-35%, and diesel at 5%, with plug-ins and battery electric accounting for 3% in total. Japan’s Government is famously responsive to its national champions - and with Toyota worth five times the amount of its decrepit former rivals, there’s only one really one domestic automotive champion worth listening to.

Europe

The trade body cartel isn’t really able to explain April’s rise in battery electric registrations in a falling market so it glosses over it, referring to “a low baseline”. But this isn’t a single month or a single country distorting the picture. Across the whole of Europe in April, only 5 countries (Estonia, Hungary, Luxembourg, Malta and Romania) saw a decline in battery electric registrations on April 2024 levels, and battery electric registrations rose 34%. In the year to date, only France, Malta and Romania saw a fall on the same period in 2024, and overall registrations are up 26%.

Meanwhile the plug-in hybrids, which some manufacturers are so desperate to sell after 2035, were outsold 2-to-1 to battery electric and have risen by just 8% in the year to date. For the conspirators and incumbents, registrations are sadly way below where they need to be for this to be a persuasive delaying tactic.

Germany’s recovery from its end-of-2023 sales crash is almost complete. Before the unplanned withdrawal of all incentives following a legal challenge on the transfer of funds to a climate and transformation fund, plug-ins accounted for 30%. Last month they were within touching distance of that total, at 29%.

In France, the sideways drift of battery EVs continues, with market share clocking 18%, in the dead centre of the 16-20% range that BEVs have tracked since August 2023. Meanwhile the death of petrol continues apace - accounting for just 22%, the lowest in Europe outside the Nordic and Benelux countries, with no sign of levelling off.

Likewise battery electric in the Netherlands is steady at 35% too whilst petrol and diesel lose market share even amongst the sceptics and laggards - they now account for just 16% of registrations and at present rates will be gone by 2027.

Spain enjoyed a sixth month in a row with battery electric market share of 6% of above, this month accounting for 6.5%. Italy in contrast saw registrations slide back to 4%, a six month low. These particular early adopter markets are still waiting to be tapped.

Outside the EU and with its own decarbonisation standards, battery electric took 20.4% market share in the United Kingdom in April, up from 16.8% achieved in the same quarter last year. With the expanded flexibilities announced but not yet introduced by the UK Government, it looks as if manufacturers are within 2 percentage points of meeting the 2025 Zero Emissions Vehicle target. They were considerably further away from the 2024 target at the same point last year and nevertheless comfortably exceeded it.

Top manufacturers

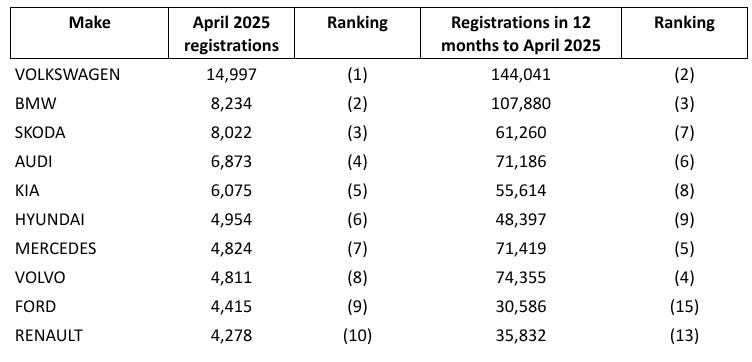

Last month we said - following better March registrations for the firm - that people might not mind Tesla so much after all. We were wrong. For the markets where we have carmaker data (the UK, Germany, Italy, Spain, the Netherlands and 4 smaller economies), Tesla performed so poorly they didn’t even make the top 10. BMW and VW Group’s Skoda marque outsold it by 2 to 1. The VW marque outsold it by 4 to 1. The Model Y is available to ship now. People aren’t buying.

Volvo and Mercedes continue to drift downwards, whilst Skoda, Kia and Hyundai have risen up the table. Meanwhile the stunning turnaround in Ford and Renault’s electrification journey continues. Both were floundering last year, with a shortage of models - now they’re in our top 10.

Who knows, Ford’s on-off love affair with zero emission vehicle regulation may be back on again. And Luca De Meo may not mind the logic of “if you don’t measure up, you pay a fine” so much, now that Renault is measuring up pretty well.