Petrol and diesel car sales stall as electric cars continue to pick up pace

Global EV Tracker: Insights from 40+ markets accounting for 85% of car sales.

Welcome to the tenth monthly issue of New AutoMotive’s Global EV Tracker. This mail offers a summary of battery electric car sales up to the end of October 2024.

For more information, you can check out the Global EV Tracker dashboard - which allows you to produce customised analysis of car sales, market share and manufacturers - at the button below. Our new country profile pages, offering an overview of country-by-country policies and sales, are available at the same link.

You’re receiving this because you signed up to receive updates from us. Changed your mind? Not a problem, you can change your preferences or opt out of emails here.

The Headlines

In October 2024:

1.04 million battery-electric cars were sold, an increase of 108,000, or 12% on October 2023.

Adding the greatest proportion of sales was China, with an increase of 79,000, or 12% on the same month last year, whilst the US was second, with an increase of just under 20,000 or 22%.

Several European markets also chalked up impressive increases, with the UK registering 5,000 more sales - an increase of 23%. Meanwhile amongst smaller markets, Belgium and Norway saw sales rise more than 30%, Bulgaria and Cyprus registered increases of more than 50%, and Denmark, Croatia, Czechia, Greece and Malta all achieved increases of more than 80%.

Roughly equal numbers of markets saw rises and falls in registrations, but amongst the largest 10 markets, only 3 - France, Germany and Sweden - declined.

Meanwhile, helped by the recent surge in Chinese plug-in hybrid volumes, vehicles with a plug now account for 25.7% of cars - more than one in four, and up from 21.9% last October.

In the 12 months to October 2024:

10.8m battery-electric cars were sold, an increase of 1.1m or more than 11% on the 12 months to October 2023. The increases were primarily driven by China, which saw new battery electric sales rise 870,000, and the US, which achieved 150,000 additional sales.

The combined market share of battery electric and plug in hybrid cars was 22.9% (up from 19.9% in the preceding 12 months).

Historical EV Sales Growth

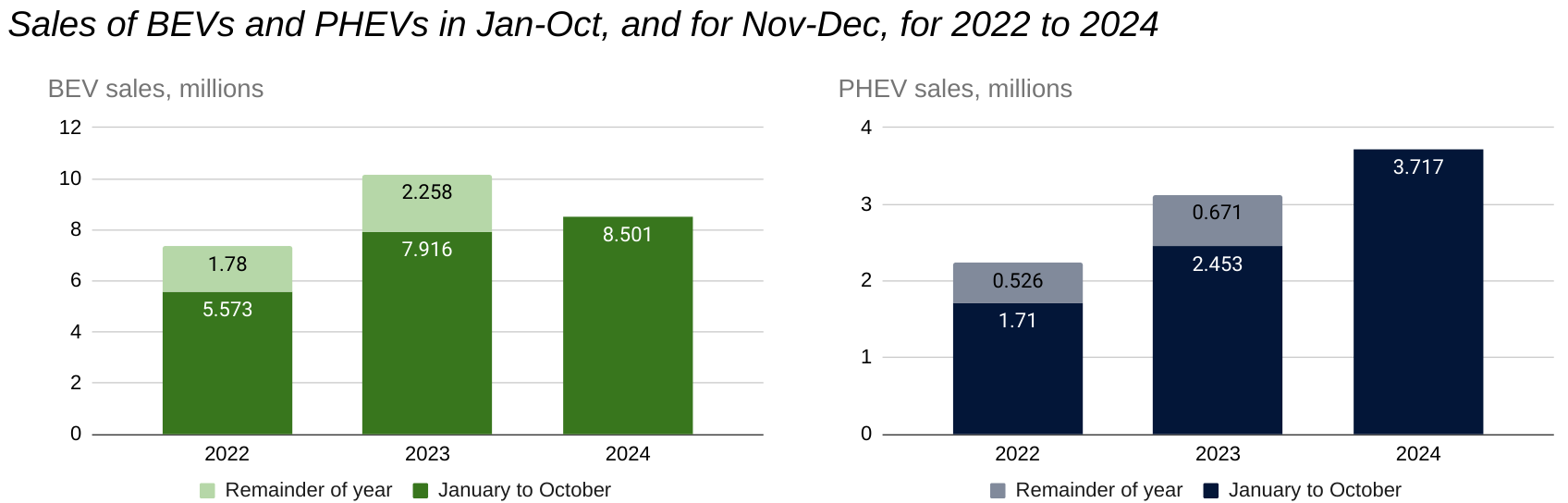

Battery electric sales are 7.4% ahead of the same point reached in previous years, whilst the smaller plug-in hybrid market is already up 32% in the year to date on the level of registrations achieved across the whole of 2023.

In contrast the market share of vehicles without a battery is in steep decline, falling from 78% to 63% - a decline of a fifth - in two-and-a-half years, and showing no sign of abating. In the same period battery electric has almost doubled its market share from 10% to 17.4%, with the remainder made up of plugins and other hybrids.

Market Indicators

What are the biggest markets for EV sales?

The 10 biggest EV markets, both in October 2024 and in the 12 months to October 2024, are shown below.

China and the US are the two largest markets for EVs, as they are for other vehicles. After a record-breaking few months, the UK has now overtaken a faltering France to become the fourth largest market.

Benelux and Scandinavian countries make up the next 5 places in the top 10 after strong sales in recent months.

BEV sales and international ranking for last month and last 12 months

Where are we seeing the greatest growth?

The emerging markets of Brazil and Chile continued their rapid growth, whilst Mexico has faded.

Smaller central and eastern European economies account for 6 of the other 7 fastest growing markets in October 2024, when measured against October 2023 levels. Many of these are small markets, but with the exception of Croatia, their boom has now been sustained for a year or more. Denmark, the other economy in the top 10, is continuing to show rapid growth, despite already reaching an EV market share of more than 60%.

Which markets have been slowest?

Amongst the worst performing economies, Romania is still suffering from a hangover after skipping EV Incentive Policy 101 and withdrawing incentives in one fell swoop. Meanwhile Iceland continues to wrestle with the outcome of introducing road pricing for all its cleanest vehicles with no policy in place to replicate it for petrol and diesel cars - cueing a collapse in buyer confidence.

Thailand’s market turmoil is a result of a 50% fall in total cars since January, which has seen battery electric hold its share better than other fuel types.

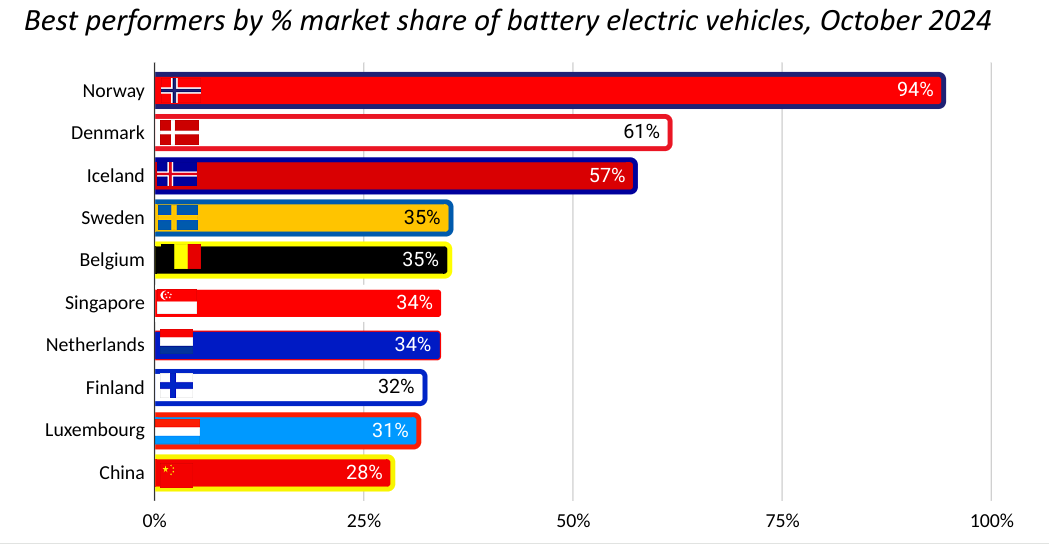

Where is EV market share highest?

The Nordic and Benelux nations hold 8 of the top 10 placings for market share in the past month, having reached well into early majority audiences with generous and (Iceland excepted) stable domestic incentive regimes.

China is by far the biggest market in the top 10.

The UK was the best performing of the big 5 European economies last month, finishing 14th highest, with 20.8% market share, after Malta, Portugal and Ireland.

Continent Analysis

Americas

US battery electric car sales were up again this month, exceeding 110,000 for only the fifth time, whilst vehicles with a battery driving the wheels exceeded 20% market share for the fourth month in a row. We expect to see a significant rush towards new battery electric in the final two months of 2024 as buyers race to beat the expected withdrawal of tax credits by the incoming Trump presidency.

What happens after that point will depend on two things - the extent to which California and other participating states are able to continue their clean vehicle mandate in face of hostile litigation; and the extent to which the EVs produced in new IRA-supported plants - and vigorously defended by Republican congressmen and women in their home states - will find willing buyers in the face of the technology’s demonisation by the President-Elect.

Whatever happens, the global switch isn’t ultimately dependent on the US. Had we seen a 50% decline in the US EV market this year - rather than a steep rise - we would still have been on course for a record-breaking 2024 for battery electric sales.

Turning to Central and South America, Chile’s battery electric bounce continues, with October’s 2.6% market share and 492 unit sales - each only exceeded once before, back in June. This is a small market, buying fewer new cars than Czechia, but it is outperforming the other Latin American countries in our study.

Brazil’s battery electric sales enjoyed a slight revival in October, exceeding 6,000 for the first time since April, but in a rising market, the share of BEVs remains stuck at 2%, half the rate reached earlier in the year.

Mexico also saw limited progress, with market share stuck at a stubborn 1.5%, as tariffs on the dominant Chinese industry increased to 20%. Mexico’s immediate EV adoption future hangs in the balance, as pressure mounts from North American trade partners to increase tariffs further.

Asia

ICE vehicle sale market share fell again in China last month, reaching a new low at 54%. The sale of plug-in hybrids continues the surge which began this year, assisted by a generous scrappage scheme to reach a new high of 18%. Meanwhile battery electric market share held steady at 28%. In a growing car market, this means that they have hit a new high, at more than 7.1 million annual sales.

The Thai car market fell for a fifth consecutive month, with petrol and diesel falling furthest. However full hybrid vehicles continue to be the main beneficiaries here. Vehicles with a battery driving the wheels now account for 40% of market share, double the level seen at the start of 2023, but only around a third of these are battery electric.

India’s headlong rush from improved air quality continues, with sales of diesel cars reaching a post-pandemic high, and plug in cars drifting dangerously, with market share of battery electric dwindling further to a two year low of 1.0%.

Taiwan’s promising run of sales from July to September ended with a slip back to 8% again in October. However this is its best ever October, in an exceptionally uneven market, almost entirely dependent on imports.

Meanwhile Singapore reached 34% battery electric market share in October, the fourth time in 2024 in which BEVs have accounted for more than one-third of sales. Chinese makers are beginning to out-compete other brands here, with first-placed BYD outselling Tesla by 2 to 1, and 5 other Chinese-owned brands in the top 10.

Japan’s transition may not be dead, but it certainly smells funny, with just 2% of vehicles sold in October using a plug, a figure which is unchanged in 5 years. That’s fine from the perspective of the Japanese Government’s under-powered climate commitments to only phase out pure petrol and diesel vehicles - these have fallen from 63% to 37%. The only difficulty is that Japanese makers depend heavily on exports and without a domestic market moving in line with the global shift, they risk being left high and dry by the transition. Nissan’s 90% fall in profits in the first half of 2024 is just an early indicator.

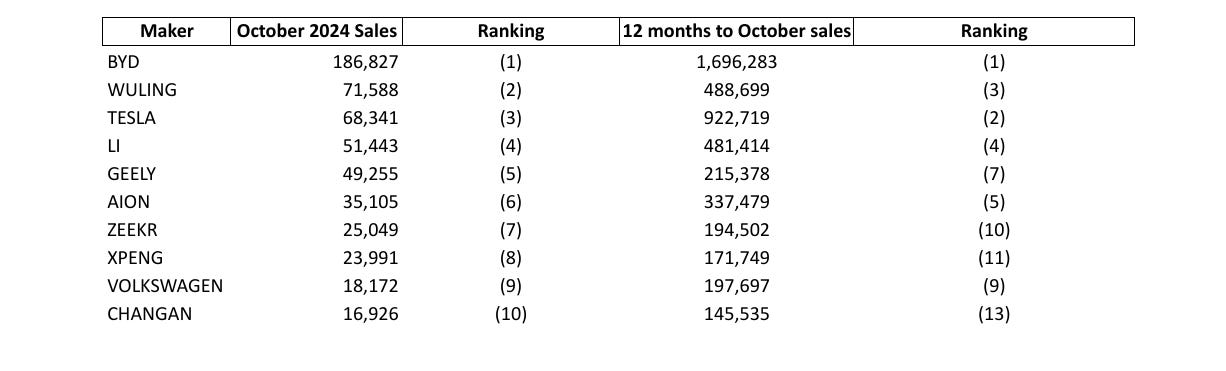

Top manufacturers

BYD outsold Tesla almost 3-to-1 in October in China, with their second best ever monthly sales total. This is just 3,000 behind their best ever result, seen in December 2023. Wuling outsold Tesla too this month, but the US manufacturer will comfortably hold onto its second place over the whole of 2024.

VW’s position in 9th is more precarious. Zeekr, in 10th, have outsold them for each of the past 3 months, and XPeng, in 11th for the last two. The next highest placed non-Chinese firm is BMW, clinging on in 19th with 1% of the market, to VW’s 2.5%.

Europe

European sales continue to stutter, with trade bodies doing their best to talk down the market in an effort to renegotiate targets which they’ve had 5 years to prepare for. With these efforts wisely rebuffed by incoming Commissioners we expect continued low EV volumes in November and December, with a renewed focus on selling EVs set to commence when tighter emission requirements kick in in January.

That said, EV buyers in Europe are doing their best to even up demand, with sales increasing steeply in many markets which were traditionally slow-moving. Bulgaria, Croatia and Czechia have now broken out well beyond the first 2.5% innovators and are finding EV buyers amongst early adopters on their domestic adoption curve. Only Slovakia is now stuck at less than 4%. And 12 European economies in the EEA - the UK, all 5 Nordic nations, the Benelux countries, Portugal, Switzerland and Malta - are all now regularly recording more than 20% battery electric market share.

Nevertheless 4 of the 5 largest economies - Germany, France, Italy and Spain - are still struggling to get moving. Germany’s glacial turnaround continues, with a third consecutive month in which sales of vehicles with a plug exceed 20%, but only two-thirds of these are battery electric. France’s car market has seen sales of all fuel types underperforming for 4 months, whilst Italy and Spain are in danger of falling behind most of Central and Eastern Europe.

Top manufacturers

Top manufacturers for the European markets for which we have data (including the car markets of Germany, the UK, Italy and the Netherlands, plus 4 smaller markets) is shown below. Tesla still leads, and will be top manufacturer for 2024. And despite a poor October, its market share is holding steady in the medium term, with the US brand accounting for 14.3% of sales in the first ten months of 2024, compared with 14.1% in the whole of 2023.

Elsewhere in the top 5, BMW have jumped forward a little over the same timescale, from 7.7% to 8.9%, whilst VW have slipped backward from 10.7% to 9.3%. The big gainers until recently have been Volvo, doubling their market share from 3.8% in the whole of 2023 to 7.6% in 2024 to date. Sales have slipped back in the face of tariffs, but Volvo is expanding production of its EV range in Ghent, Belgium, where the tariffs won’t apply.

On the subject of tariffs - we still haven’t seen a month where the duties will apply. The EU imposed provisional duties on 4 July, but its final decision on 29 October indicated that these will not be collected.

But now that the expectation of tariffs has now weighed on some manufacturers for 4 months, it is interesting to compare the changing market share of the top Chinese manufacturers in the EU with the UK, which has not imposed tariffs.

As the charts below show, MG and Volvo’s share of the BEV market actually increased in the EU with the announcement of the tariffs - possibly by bringing forward imports - and total market share remains above the level when the competition review was announced. Meanwhile in the UK, market share has always been higher - chiefly due to the popularity of the MG brand - and has shown no sign of increasing as competitors cut costs to meet the UK’s zero emissions vehicle mandate.

Time will tell whether the EU’s tariffs will be worth the pain inflicted on its domestic firms who make some of their EVs in China. But so far, the UK’s ambitious supply-side regulations appear to have done a better job of prompting traditional manufacturers to raise their game and boost their market share.