Sales climb despite German slump, as US hits record highs and China plug-in demand broadens + Webinar

Global EV Tracker: Insights from 40+ markets accounting for 85% of sales.

Welcome to the eighth monthly issue of New AutoMotive’s Global EV Tracker.

This mail offers a summary of battery electric car sales up to the end of August 2024. Don’t forget you can check out the full country-by-country report, as well as the Global EV Tracker dashboard, which allows you to produce customised analysis of sales, market share and manufacturers at newautomotive.org/global-ev-tracker.

Let us know what you think of this new format at general@newautomotive.org.

We are hosting a webinar on Thursday 24 October 2024 for a first look at the 3rd quarter set of results from New AutoMotive’s Global Electric Vehicle (EV) Tracker - we would love to have you there!

The Headlines

In August 2024:

861,500 battery-electric vehicles were sold, a decrease of 63,000, or 6.8% on August 2023. This was almost entirely due to the continued failure of the (3rd largest) German market to recover from the sudden withdrawal in incentives at the end of 2023, leaving monthly sales 60,000 lower last month than they were last August.

The largest market, China saw an 81% surge in the sales of plug in hybrids on the previous August, at the expense of a 3% downtick in battery electric and an 18% slump in internal combustion engine cars. Meanwhile the US, as the second largest market for EVs, reached more than 120,000 monthly sales, its highest for 2024 and second best of all-time.

17 markets saw an increase in sales on August 2023 levels. Whilst 25 markets - mostly smaller markets - declined, overall sales excluding China and Germany were up 6.2%.

16.3% was the battery electric market share - down 0.5 points on August 2023 - again due to the steep fall in the German market and the recent PHEV surge in China.

Nearly one in every 6 vehicles sold was fully electric.

In the 12 months to August 2024:

10.60m battery-electric vehicles were sold, an increase of 13.0% on the previous 12 months, with the increases primarily being driven by China and the US.

30 markets - including 8 of the 10 largest EV markets - saw sales increase on the previous 12 months, whilst Germany and 10 smaller markets saw a decline.

15.8% is the battery electric market share (up 1.1 points on the preceding 12 months).

More than one in seven vehicles sold were fully electric.

The Third Global EV Tracker Webinar

Please join us on Thursday 24 October 2024 for a first look at the 3rd quarter set of results from New AutoMotive’s Global Electric Vehicle (EV) Tracker.

In our 3rd instalment, we will present an in-depth analysis of charge point rollout, with a particular focus on the UK and Europe.

Alongside this, we’ll provide our signature global electric vehicle sales and analysis for Q3 2024, examining the data to forecast trends for the remainder of the year. We’ll highlight which countries are leading in EV adoption, explore the policy incentives driving this growth, and offer insights into market share trends and key manufacturers, including the impact of tariffs.

Date: 24 October 2024

Time: 12.30 – 1.30 pm (BST)

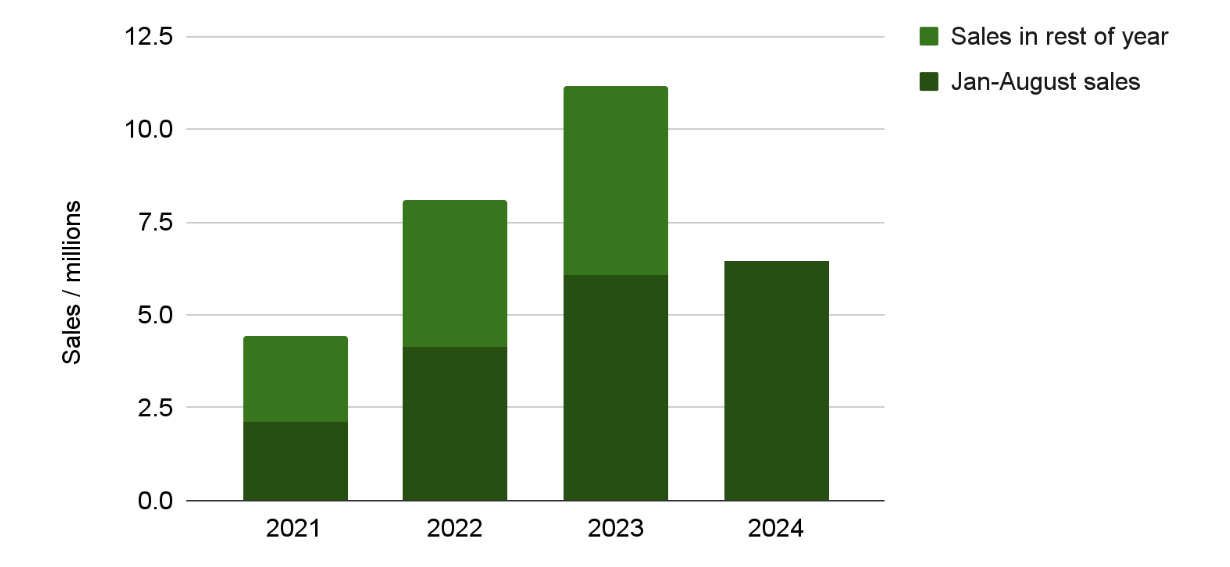

Historical EV Sales Growth

EV sales are currently ahead of the same point for previous years.

Market Indicators

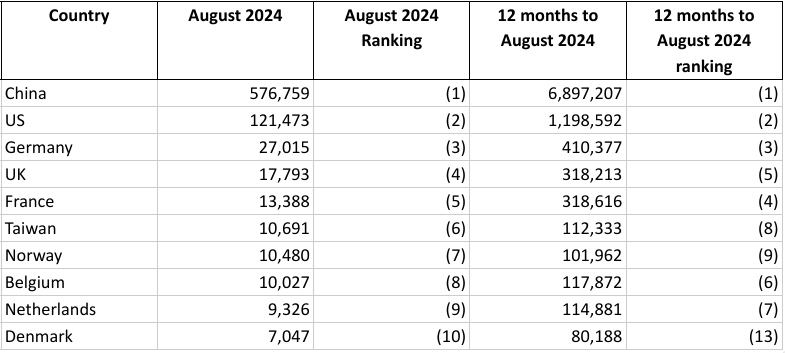

What are the biggest markets for EV sales?

The 10 biggest EV markets, both in August 2024 and in the year to August 2024, are shown below.

China and the US are the two largest markets for EVs, as they are for other vehicles. Continued outperformance by the UK means it could well overtake France as the 4th largest market for 2024. Taiwan is the 3rd largest non-European market in the world, but Turkey, Thailand and India also sit just outside the top 10.

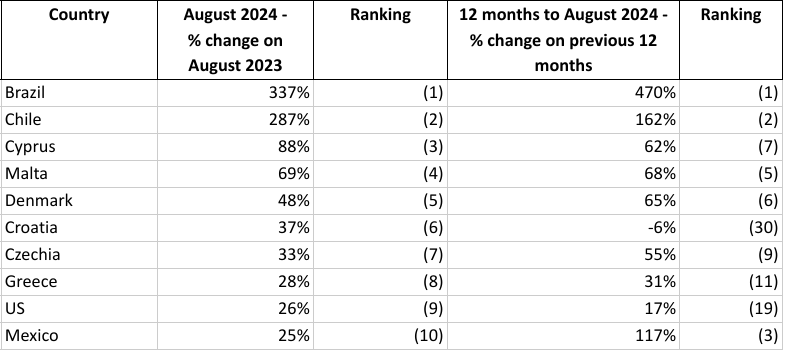

Where are we seeing the greatest growth?

Emerging markets of Chile, Brazil and Mexico continue to hold the top 3 places in the medium terms with sales more than doubling in the 12 months to August 2024 on the previous year. However each fell back on July 2024 levels.

Smaller Eastern and Southern European economies hold 5 of the other places in the top 10, but Cyprus, Malta, Denmark, Czechia and Greece are all showing consistent strong growth.

Most interestingly, the US gives the lie to stories of a slowdown, with sales up 26% in August 2024 on the same month in 2023, and a solid increase of 17% over the past 12 months. The UK saw a 10% increase in August 2024 sales on August 2023 levels.

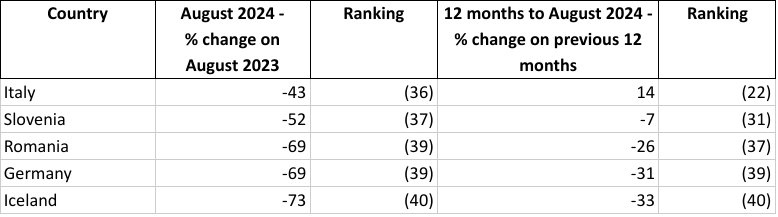

Which markets have been slowest?

Amongst the worst performing economies, Romania, Germany and Iceland have all seen dramatic or chaotic withdrawals in consumer incentives, alongside the additional introduction of EV-only road pricing in Iceland. Meanwhile Italy’s poor placing shows the after-effects of a short term round of grants which was exhausted in less than one day. All these countries’ experiences demonstrated the importance of policy stability - rather than stop-go grant giving - to maintain consumer demand.

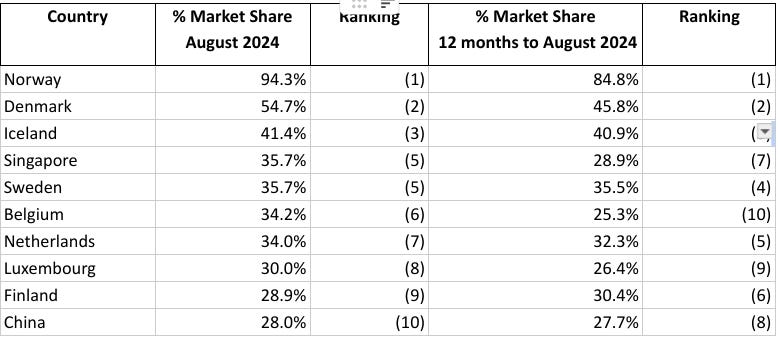

Where is EV market share highest?

The Nordic and Benelux nations hold 8 of the top 10 placings for market share, with Iceland still holding onto 7th, despite the disastrous introduction of road pricing for clean vehicles. China is by far the biggest market in the top 10, with the other non-European place occupied by the city-state of Singapore.

The UK recorded 12th highest market share in July 2024, at 23.1%.

Continent Analysis

Asia

ICE vehicle sales in China continue to tank - falling 18% in August 2024 on August 2023 levels. Plug in hybrid and range extended vehicles captured all of that decline and ate slightly into battery electric market share last month. With a PHEV market share of 16.6%, China is now only just behind the Nordic leaders of Sweden, Finland and Iceland in the adoption of this technology. PHEV uptake may be a result of electrification reaching out to more rural areas, where concerns about the availability of charging are more salient, or a response to rapid cuts in the prices of PHEVs relative to ICE alternatives.

Thailand continues to surge, reaching 15% battery electric market share - its second best result of 2024. Here plug-in hybrids have made less impact, and the collapse in petrol and diesel sales - from 73% in August 2023 to 56% last month - is being absorbed by plugless hybrids alongside battery EVs.

Turkey’s market remains volatile, with total car sales down 40% on July 2024 - a fall which appears not to be seasonal. Battery electric market share held up at 9%, but petrol saw a one month fall in share from 65% to 54%. It will be interesting to see if this drop off is maintained.

In India sales continue to dip, as Ministers make worrying noises about incentives to switch becoming unnecessary. This is misguided. BEV market share is at its lowest level since February 2023, with alternative fuels and - despairingly, given India’s air pollution levels - diesel the only fuel types to see sales increase on August 2023 levels.

In better news, Singapore continued its rapid progress, reaching a new battery electric high of 36%. With PHEVs almost completely absent, however, 64% of new cars sold in August remain mainly reliant on petrol, a position China broke through in March of this year.

Taiwan’s high volumes of vehicle purchase placed it in the top 10 EV markets this month, despite battery electric accounting for only a 10% market share. This is its third best result of 2024, and better than every month of 2023, but sales are still operating in the 5-15% band seen since 2019.

Finally Japan remains stuck in an even lower band, with just 1.4% market share over the past 12 months. This month it was beaten by the much poorer Indian economy, only exceeding Chile and Mexico.

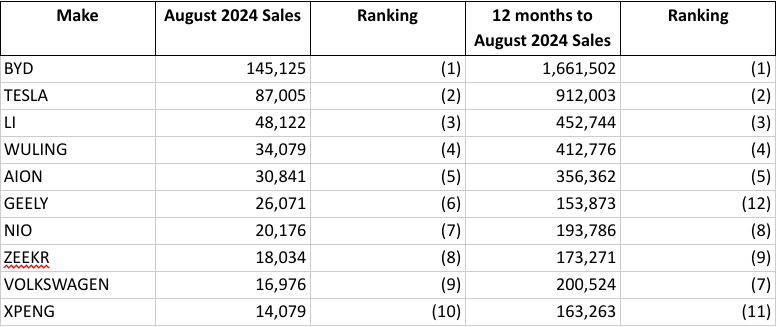

Top manufacturers

The Chinese market is so huge compared with the Singapore and India markets - the other Asian markets for which we have manufacturer data - that the top 20 for Asia is the top 20 for China. BYD and Tesla pulled ahead of other manufacturers this month with Tesla adding 12,500 sales, whilst BYD added 18,800. The other big riser was Geely which leapt into the top 10 with its best selling month since we began to collect data.

BMW (15th) and Toyota (19th) cling on, but both saw sales dip. There are no other European or Japanese EV sellers in the top 30.

Europe

Europe’s run of self-made madness continues. Compounding weak EU-wide emissions targets, reach-10%-cancel-and-repeat incentive schemes, the imposition of self-destructive tariffs on many of their own biggest manufacturers in July will make many home-grown models more expensive and damage confidence.

August’s latest genius move is to task the new EU climate commissioner with amending the CO2 emission performance standards to create a role for inefficient non-existent e-fuels. Simples.

Outside the EU, the story is better, with Norway, months away from its ban on ICE vehicles, scoring 94% EV market share.

The UK also had a strong month, recording 23% market share, the highest since December 2022. This came despite the new administration’s support for the switch being currently limited to rhetoric on ending the sale of pure petrol and diesel - and presumably some hybrid - vehicles in 2030. Car buyers note the direction of travel, and the UK’s much better designed regulation does the legwork to boost market share, without stop-go incentives.

There are bright spots in the EU - Belgium scored an all time high of 34% market share for battery EVs, whilst Denmark hit a new high of 55%. Meanwhile around one in three cars sold in the Netherlands, Sweden, Finland and Luxembourg are battery electric, with further substantial sales of PHEVs in Sweden and Finland.

France continues to slide - reaching 15.4% battery electric market share, its second worst result of 2024. However Germany’s long slow comeback is back on track after its second best month of sales in 2024, although at 13.7% this places it 16th in Europe - just ahead of Cyprus and a little behind Malta.

Elsewhere in smaller European EV markets, Cyprus (9.5%), Greece (6.3%) and Croatia (6.1%) all achieved their second best month for market share ever, whilst Switzerland reached 21.5%, its second best result of 2024.

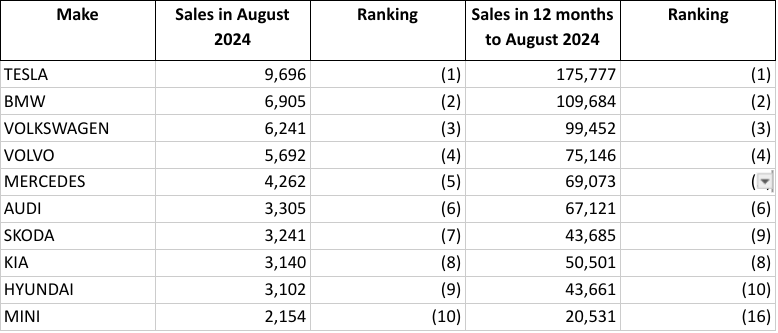

Top manufacturers

Top manufacturers for the European markets for which we have data, including non-EU states, is shown below. Tesla took its number one placing back from BMW in August 2024. The lack of new models from the US firm whilst competitors innovate is cutting its market share, but Tesla will comfortably top the market this year. Whilst Geely-owned Volvo comfortably holds its fourth place, fears of a Chinese takeover are over-egged. MG has fallen out of the top 10, its place taken by the German-owned (but sometimes China-built) Mini.

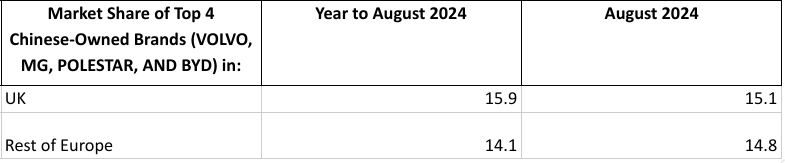

To estimate the effect of the EU’s tariffs on vehicles sold by Chinese firms, which have not been replicated by the UK, we show the market share of the top 4 Chinese-owned firms, in the two jurisdictions.

The analysis suggests that the tariffs have so far have limited effect. The market share of EVs produced by Chinese-owned makers in the EU for August remains above the 12 month average - although time will tell whether this is due to the influx of vehicles before the tariffs began to bite in early July. Meanwhile in the UK, Chinese manufacturer market share has continued to flatline, even falling back slightly on July’s figures.

Americas

The US had its best month of all time for battery electric market share, with 8.6% and its second best ever month for sales, with volumes exceeding 120,000 - beaten only in December 2023. It may be that we will see a strong few months as buyers rush to take advantage of tax credits, ahead of a possible Trump victory and the promised gutting of the Inflation Reduction Act. Petrol vehicles also had only their second ever month of below 80% market share, a record reached for the first time last month.

So large is the US market, that even with a market share in single figures, more battery electric vehicles were sold there in August than in the 18 largest European markets.

Turning to Central and South America, Brazil managed to prevent a fifth consecutive month of declining market share, but sales are still below levels reached in June.

Chile’s nosedive continues, recording market share of 1.1%, lower than any month since February 2024. Meanwhile Mexico scored a similar 6-month low, only slightly higher at 1.35%. Whilst Brazil’s slide is more likely connected with new taxes, we remain hopeful that the recent slides in Chile and Mexico are blips, wich will soon be reversed.